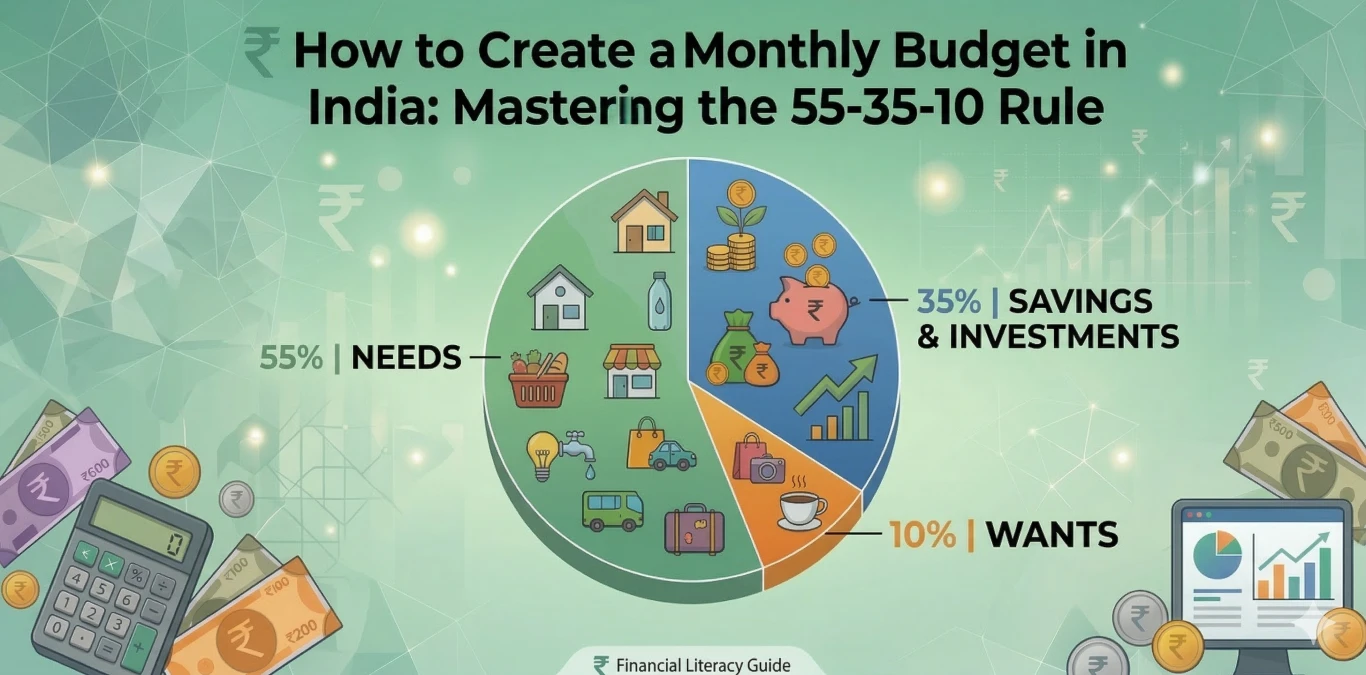

In our previous post, we laid the essential groundwork for taking complete control of your family’s finances. We broke down the core components of an Indian household budget and introduced the powerful 55-35-10 Rule. This is a highly realistic framework designed specifically for our unique wealth-creation needs.

(If you missed that foundational guide, I highly recommend reading it first so you can set up your basic percentages correctly. [Click here to read it here: The Foundation & The 55-35-10 Rule])

Now that you have your core percentages locked in, it is time to elevate your financial game. Knowing how much to save is only half the battle; knowing how to actually stick to it in a modern world of frictionless UPI payments, 10-minute grocery deliveries and sudden family obligations is where the real magic happens.

In this second part of our ultimate budgeting guide, we dive into innovative daily budgeting hacks to tame the digital spending trap, uncover the most common financial mistakes Indian families make and share the best tools to simplify your journey to total financial freedom.

Let’s dive right into the advanced strategies!

Budgeting Techniques to Try Today

If a standard percentage spreadsheet feels a little too theoretical at first, there are several distinct budgeting philosophies you can adopt to manage your daily cash flow. Choose the specific one that best fits your personality and your psychological relationship with money.

Zero-Based Budgeting (Every Rupee Has a Job)

Zero-based budgeting is not a separate type of budget; rather, it is the exact technique you may use to practically enforce your 55-35-10 rule. The core concept is simple: your monthly income minus your allocated categories must equal exactly zero.

This absolutely does not mean you spend everything; it means you intentionally assign every single rupee to its designated percentage bucket before the month even begins.

For example, if you earn ₹50,000, you assign every single rupee a specific job across your three categories on the 1st of the month:

- Income: ₹50,000

- Essential Needs (55%): – ₹27,500

- Savings/Investments (35%): – ₹17,500

- Wants/Lifestyle (10%): – ₹5,000

- Remaining: ₹0

This execution method is incredibly effective for Indian families who suffer from “leaky wallet syndrome”—where thousands of rupees simply vanish from the bank account each month, and no one knows where it actually went. By assigning every rupee a strict job within your 55-35-10 framework, you entirely eliminate mindless, wasteful spending.

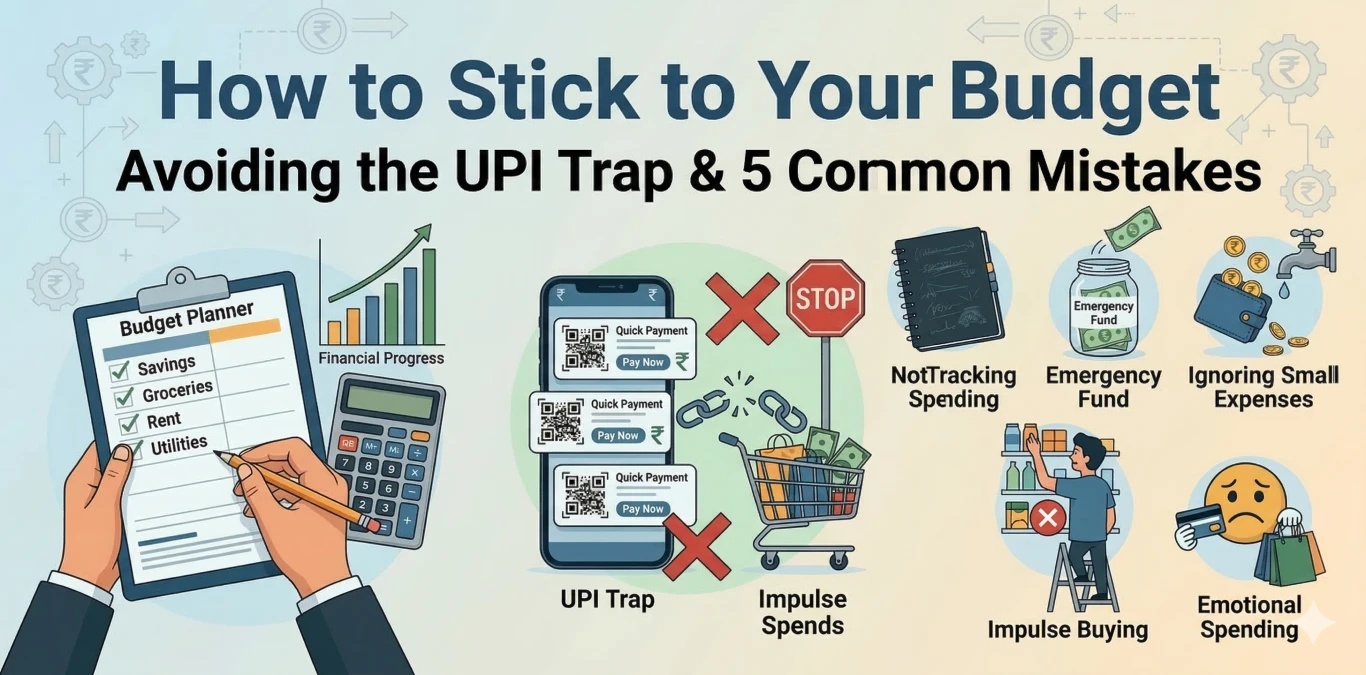

The Two-Account System (Avoiding the UPI Trap)

In India, digital payments have fundamentally changed how we handle money. You scan a QR code for a ₹20 cutting chai or a ₹2,000 weekend dinner with the exact same ease. The physical friction of exchanging cash has completely vanished.

So, what happens when you hit your 10% “Wants” threshold by the 20th of the month? You cannot simply uninstall BHIM-UPI or any online payment apps. Because you still need them to pay for your essential 55% “Needs” like groceries or electricity bills.

Instead of deleting your apps, you can create a brilliant digital boundary:

- The Salary vs. Spending Accounts: Never link your primary salary and savings account to your daily UPI apps. Instead, maintain a secondary, basic savings account (many banks offer zero-balance accounts). At the beginning of the month, transfer only your allocated monthly spending funds (your Wants and daily variable Needs) into this second account and link your daily UPI strictly to it. When the funds in this secondary account dry up, your QR scans decline. You hit a hard, uncrossable boundary without ever putting your rent or emergency funds at risk.

- Utilise UPI Lite or Digital Wallets: If opening a second account feels tedious, use the “UPI Lite” or wallet features available in most major payment apps. You may load your exact entertainment or dining budget into this specific wallet. Once the wallet balance hits zero, you must consciously stop spending.

- Adjust Bank-Level Limits: Almost all modern Indian banking apps allow you to instantly modify your daily UPI transaction limits. If you realise you are nearing your monthly spending limit too fast, you can simply log into your core banking app and temporarily drop your daily UPI limit. It adds just enough friction to completely stop the impulse to order online, which is above the limit.

The Hybrid Method (Cash for “Wants”, UPI for “Needs”)

If tweaking bank limits or opening secondary accounts feels like too much work, you may try a simple hybrid approach. Keep your UPI active strictly for your essential, non-negotiable bills like paying rent, the electricity bill or your core kirana run. However, for your 10% discretionary “Wants” (like cafes, weekend movies or casual shopping), withdraw that exact amount in physical cash on the 1st of the month. When you go out for entertainment, rely only on the cash in your pocket. It beautifully brings back the physical “pain of paying” that frictionless digital payments have erased. Once the cash runs out, your entertainment budget is officially closed for the month and you cannot fall back on scanning a QR code.

The Cash Envelope System (The Old-School Approach)

Our grandparents used this exact method and it still works phenomenally well today, especially for variable discretionary expenses. If you constantly overspend on groceries, eating out or personal care via UPI, switch entirely to physical cash for these specific, problematic categories.

At the very beginning of the month, withdraw your 10% “Wants” budget in cash from the ATM. If your Wants budget is ₹5,000, put it in an envelope. When you go to a restaurant or the local market for non-essentials, only take cash from that specific envelope. When the envelope is empty, the spending completely stops until next month. No exceptions and no scanning QR codes. It adds immediate physical friction to your spending, which digital payments have entirely removed from our brains.

Common Budgeting Mistakes to Avoid

Even with the absolute best intentions, families often stumble when creating their first few budgets. Watch out carefully for these highly common Indian budgeting pitfalls:

1. Setting Unrealistic Restrictions

If you suddenly stop spending on entertainment and dining out completely, you’ll likely end up overspending later. Let’s say, for example, if you currently spend more than 10% a month on eating out, don’t drop it to zero. Cut it realistically, then slowly, to your target 10% over a few months. Give yourself and your family some breathing room to actually adapt to the new lifestyle.

2. Not Budgeting for Family Responsibilities

In India, families are deeply interconnected, both emotionally and financially. We often help out ageing parents, contribute heavily to a younger sibling’s college tuition or pitch in unexpectedly for a medical emergency of an extended relative. If you know you regularly send money to your family, make it a permanent, formal line item in your “Essential Needs” monthly budget. Do not let it disrupt your own core financial stability.

3. Ignoring the Vital Emergency Fund

Do not start aggressively investing heavily in the stock market or pre-paying your home loan if you do not possess an emergency fund first. A proper emergency fund contains 3 to 6 months’ worth of essential living expenses sitting safely in a highly liquid instrument. If a sudden illness strikes or a job is temporarily lost, this specific fund is your family’s financial oxygen mask.

4. Confusing Insurance with Investment

Many Indians still buy traditional endowment policies or ULIPs (Unit Linked Insurance Plans) thinking they are “investing” while getting life cover. These hybrid products often give sub-par returns (barely beating inflation) and offer drastically inadequate life cover for your dependents.

The Fix: Buy a pure Term Life Insurance policy for massive protection (it is incredibly cheap if bought early) and invest the remaining difference directly into Mutual Funds or PPF for actual wealth creation. Keep your insurance and your investments strictly separate in your financial planning.

5. The “Set It and Forget It” Trap (Failing to Review and Revise)

Many people treat a budget like a one-time school project. You might spend hours making a perfect, beautiful plan for January, but by April, you are still trying to use those exact same numbers. You create it for the first month, put it in a drawer (or close the app) and never look at it again to see what actually worked and what completely failed.

Life in India is highly seasonal and constantly changing. Your electricity bill will naturally double in May due to summer AC usage. October and November will demand a much higher “Wants” and “Gifts” budget because of the festive season.

If you do not review your budget at the end of every month, you miss the opportunity to learn from your mistakes. If you constantly overspend your 10% limit on weekend cafes, your budget isn’t broken—it just needs an adjustment for reality.

The Fix: Treat your budget as a living, breathing document. Schedule a “money date” on the last Sunday of every month. Budgeting should never be a stressful secret kept by one person. You should involve your spouse and children in a monthly “money date” to transform financial planning from a heavy burden into an exciting team effort. You should sit down together, order some snacks and openly discuss the upcoming month’s goals, like saving for a weekend trip or a festival.

For children, this process is the ultimate financial education. Why not introduce basic concepts of saving to a toddler using a physical piggy bank or give older kids a small, fixed “Wants” budget to manage themselves? Involve them in this journey so they can become confident and good with money. This way, budgeting will feel like a normal part of life instead of a scary task.

Tools and Resources for Budgeting in India

You certainly don’t need to be a maths genius or a chartered accountant to budget effectively. Technology has made it significantly easier than ever before.

- The Classic Pen and Diary: Never underestimate the raw power of writing things down manually. A simple ledger detailing “Money In” and “Money Out” is exactly how millions of highly successful Indian businesses run. It forces you to interact with your numbers.

- Spreadsheets (Excel/Google Sheets): For those who love granular control, a custom spreadsheet allows you to tweak every single percentage parameter. You can easily build your own 55-35-10 tracker tailored to your exact income.

- Manual Tracking Apps: Some apps allow you to manually input your expenses on the go. Always download and install applications only from verified sources such as official app stores.

- Modern Bank Features: Many modern Indian banks now feature built-in “Spend Analyzers” directly in their mobile banking apps that automatically categorise your daily transactions for quick review at the end of the month.

Conclusion and Call to Action

Creating a monthly budget is not a one-time, tedious event; it is a lifelong, rewarding habit. The very first month you try to budget, it may likely be messy. You may forget a crucial expense or a sudden, unexpected festival may blow your 10% “wants” category entirely out of the water. That is completely normal and okay. The overarching goal is consistent progress, not immediate perfection.

By investing time in planning your monthly budget, you move closer to financial freedom. It does not matter whether you are a high-income earner or a low-income earner. A budget helps you work toward your financial goals. In fact, it is possible to build a high net worth even with a modest income when money is managed wisely.

By truly understanding your real income, relentlessly tracking your expenses, adapting the 55-35-10 rule to our unique cultural spending habits and automating your vital investments, you take the most crucial step toward total financial independence. You actively shift your family from a stressful mindset of month-to-month survival to an empowered mindset of generational wealth creation.

Your future self—the one who dreams of retiring comfortably, travelling the world freely and providing the absolute best for your family—is going to thank you profusely for the hard work you put in today.

We Want to Hear from You!

Financial literacy grows exponentially when we openly share our experiences with one another. Budgeting in an Indian household is a distinctly unique challenge and we can all learn immensely from each other’s real-world hacks and strategies.

Drop a comment below and let us know:

- What is the absolute hardest expense category for you to control in your household right now?

- Do you have a unique “Desi Hack” for saving money (like buying bulk groceries from the local wholesale market or carpooling)?

- Which budgeting percentage formula (55-35-10 or your own custom blend) are you planning to implement this month?

Share your thoughts, join the conversation and let’s build a strong community of financially empowered households together.