If you have ever reached the last week of the month and wondered, “Where did all my money go?”, you are certainly not alone. Millions of households across India experience the same routine: salary credits arrive on the 1st of the month; UPI notifications for bills, EMIs and groceries arrive and by the 25th, we eagerly wait for the next salary credit.

We Indians have a cultural tendency to save. Our grandparents hid cash in rice jars and relied heavily on post office savings schemes, prioritising security above all else. But modern life has changed drastically. The old strategy of “spending less” or doing mental maths is no longer sufficient due to the convenience of UPI payments, the constant temptation of 10-minute grocery deliveries, simple zero-interest EMIs on the latest smartphones and the rapidly rising cost of living in both Tier 1 and Tier 2 cities.

Now that spending is completely frictionless, saving requires deliberate planning. We can no longer rely on having enough money at the end of the month. We need a clear and proactive system to manage this digital chaos. The good news is that we do not need a new invention to navigate this new financial landscape; instead, we simply need to use the best tools available. It is time to start budgeting.

A budget is not a restriction; it is a powerful financial roadmap. It is simply the act of telling your money where to go instead of wondering where it went. In this comprehensive guide, we will look at how to create a monthly budget that is tailored to the specific dynamics, cultural nuances and financial realities of an Indian household.

So, grab a fresh cup of chai, get comfortable with a notepad and let’s dive deeply into mastering your personal finances.

Understanding the Importance of Budgeting

Before we get into the “how”, we must understand the “why”. Why should you spend your precious Sunday afternoon looking at spreadsheets or tracking your expenses?

Many of us believe budgeting is only necessary when income is limited. In reality, budgeting benefits you regardless of your income level.

It helps you understand your spending patterns.

Without a budget, spending frequently occurs entirely without conscious thought. For example, think about any family’s monthly schedule. It includes:

- Weekly grocery shopping at supermarkets

- Ordering food online through delivery apps

- Eating out at restaurants or cafés

- Utility Bills

- Medical Expenses

- OTT subscriptions

Individually, these expenses seem minor. However, together they may add up to several thousand rupees every single month. A budget helps you clearly identify these spending patterns and gives you the power to adjust them if necessary.

It encourages savings and investments.

You might try to save whatever remains at the end of the month. Unfortunately, in most cases, absolutely nothing remains! A budget fundamentally changes this approach. Instead of saving what is left over, you allocate your savings first and then you manage the rest of your expenses. This simple mental shift can dramatically improve your long-term financial stability.

It Prepares You for unexpected expenses.

Like most Indian households, yours frequently faces irregular, unannounced expenses such as:

- Sudden medical emergencies

- Unexpected wedding invitations (lifafas and gifts)

- Urgent home or vehicle repairs

A budget allows you to set aside small amounts every month for these specific situations. This will prevents sudden financial strain when the event actually arrives.

It Sets a Powerful Example for the Next Generation

Budgeting is rarely just an individual exercise; it is a family activity. When you openly manage your money, you create an environment of financial literacy for your children. You can playfully explain to your young ones (perhaps when they ask for a new toy or when you sit down for a family board game like Snakes and Ladders) that money is a tool we manage carefully. Even a three-year-old watching you set aside cash in an envelope or a savings jar begins to naturally grasp the concept of delayed gratification. By managing your finances visibly, you pass down healthy money habits that can protect them for a lifetime.

Achieving Peace of Mind

One of the biggest causes of stress in households is uncertainty about money. Financial stress remains one of the leading causes of anxiety. Knowing exactly how you intend to pay your child’s upcoming school admission fees, having a substantial emergency fund set aside for unexpected medical expenses and watching your retirement fund grow provides a profound, irreplaceable sense of peace. A structured budget provides clarity. When you know exactly how much is allocated for each category, financial anxiety reduces significantly.

Key Components of a Monthly Budget

A common mistake most of us make is thinking that a budget is just a restrictive list of our spending. It is not. A well-structured budget is actually a delicate balance of three distinct pillars: Income (Money In), Expenses (Money Out) and Savings/Investments (Money Kept).

Let us understand each of these.

Household Income (Money In)

Income includes all the money coming into your household every month. Knowing your exact net income is the first step in designing a realistic budget. The sources include salary, Business or Freelancing Income, Rental Income, Pension, Interest or dividends, etc.

Household Expenses (Money Out)

The expenses of an Indian household are very different. You deal with expenses that Westerners rarely consider, such as monthly financial help to the parents living in hometown, salaries for part-time domestic help and sinking funds for a busy calendar of festivals and family weddings.

To create a highly functional budget, carefully categorise your expenses into four areas:

A. Essential Expenses (The Must-Haves)

These are the absolutely mandatory expenses required for your family’s survival, comfort and daily functioning. All of these expenses are budget priorities that cannot be negotiated. Some are fixed, meaning the mandatory bills that generally do not change from month to month. You know exactly when they are due and exactly how much they cost. While others are variable means, these are absolutely necessary expenses for survival but the exact amount fluctuates from month to month based on your family’s usage and choices.

- Housing & Maintenance: It includes your monthly rent, Home Loan EMI and Society Maintenance fees paid to your housing society.

- Groceries & Daily Needs: The monthly kirana store bill, daily milk, bread, fresh vegetables, fruits, meat, etc.

- Utilities & Connectivity: Electricity (which often spikes drastically during harsh Indian summers), water charges, cooking gas (LPG/PNG) and your essential broadband internet connection.

- Transportation: Car or two-wheeler EMIs, petrol/diesel, metro passes, cab rides or daily auto-rickshaw fares.

- Education: Monthly school fees, after-school tuition fees or school bus transport charges.

- Health & Medical: Health and term life insurance premiums, regular prescription medications for older family members, vitamins and occasional doctor consultation fees.

- Household Support: Regular salaries for your maid, cook, driver or nanny, if any.

- Personal Care: Basic toiletries, hygiene products and haircuts.

B. Discretionary Spending (The “Wants” and Luxuries)

This specific category is exactly where most household budgets fail. These are entirely non-essential expenses and the things you purchase are purely for fun, convenience, leisure or social status.

- Dining Out & Delivery: Ordering food online, having weekend dinners at restaurants or getting daily coffee from a local cafe.

- Entertainment: Weekend movie tickets, concert passes, weekend getaways to nearby resorts and shopping for non-essential trendy clothes or the latest electronic gadgets, OTT subscriptions

- Hobbies: Sports equipment, dance classes, video games or premium app subscriptions

Remember to keep track of every expense, no matter how small. These daily small expenses can accumulate quickly. Tracking these expenses often reveals surprising patterns.

C. Periodic Expenses (The Sinking Funds)

In the Indian cultural context, you cannot budget effectively without rigorously planning for annual or semi-annual expenses. Most of us often forget to include these expenses while making a budget. If you don’t plan for these specific events, they inevitably feel like massive financial emergencies when they finally arrive.

- Festivals: Diwali, Christmas, Durga Puja, Ganesh Chaturthi, Raksha Bandhan. These grand celebrations naturally involve buying new clothes, purchasing sweets in bulk, exchanging gifts and heavy home decor.

- Family Obligations: Cash gifts for weddings (lifafas or shagun), fancy and expensive gifts for close family weddings, and gifts for birthdays and anniversaries in the extended family.

- Annual Fees: Annual school admission or development fees, annual vehicle insurance renewals and municipal property tax.

- Home Maintenance: Annual home painting, AC servicing right before summer begins and inevitable appliance repairs.

Pro-Tip: The ultimate secret to seamlessly handling periodic expenses is establishing a “sinking fund”. You know you usually spend ₹24,000 a year on your car’s insurance and servicing; simply divide that amount by 12. Save exactly ₹2,000 every single month in a completely separate, untouchable savings account. When the annual bill arrives, the money is already there waiting for you.

Savings and Investments (Money Kept)

Savings protect you from emergencies, while investments help you build long-term wealth. Typical financial goals in Indian households include:

- Emergency fund creation

- Children’s future higher education and marriage planning

- Buying a house

- Retirement planning

- Wealth Creation

Even setting aside 10–20% of your income every month can create significant financial security over time.

The Step-by-Step Guide to Creating Your Monthly Budget

Let’s translate all of this financial theory into solid practice. The biggest myth in personal finance is that budgeting requires a specific, high-income level. In reality, the most successful budgets do not rely on fixed rupee amounts; they rely entirely on percentages.

By allocating your income in percentage terms, your budget automatically scales with you. If you get a promotion, your savings increase automatically. If you take a temporary pay cut, your lifestyle will decrease proportionally without causing panic.

Here are the precise steps you can take today to build a rock-solid, foolproof budget based on the power of percentages.

Step 1: The Honest Income Assessment (Finding Your 100%)

The absolute first mistake people make is budgeting based on their CTC (Cost to Company). Your budget must be based only on the actual, liquid money that hits your bank account. This final take-home amount represents your 100%.

- Determine Net Income: Look closely at your bank statement. What is the exact amount deposited after your employer deducts PF, TDS, and professional tax? That is your baseline.

- Variable Income: If you are a freelancer or a small business owner, your income naturally fluctuates. Calculate your average monthly income over the last six to eight months and then build your percentage-based budget on the lowest-earning month just to be perfectly safe.

Step 2: Expense Tracking

You simply cannot change what you do not accurately measure. Before assigning new percentages for next month, you urgently need to know exactly how your 100% was divided up last month.

Sit down with your bank statements, credit card bills and your UPI app transaction history. UPI has beautifully revolutionised payments in India, but it has also made “micro-spending” dangerously invisible. That cutting chai at the corner stall, the quick auto ride, it all adds up to a massive chunk of your income. Categorize your expenses from the last 30 days to see exactly what percentage of your income is currently leaking into non-essential categories.

Step 3: Setting Meaningful Financial Goals

A budget without a clear goal is like a journey without a destination—you eventually lose motivation and revert to old habits. Your goals give your savings percentages a distinct purpose. Categorise your family’s goals into three specific timelines:

- Short-Term Goals (0-1 year): Building a robust emergency fund (crucial for peace of mind moving forward), saving for a short family vacation or buying a much-needed new household appliance.

- Medium-Term Goals (1–5 years): saving aggressively for a down payment on a new house, upgrading the ageing family car, or anticipating the rising education costs for a growing toddler.

- Long-Term Goals (5+ years): Building a massive retirement corpus, funding your children’s higher education or paying off the heavy home loan early.

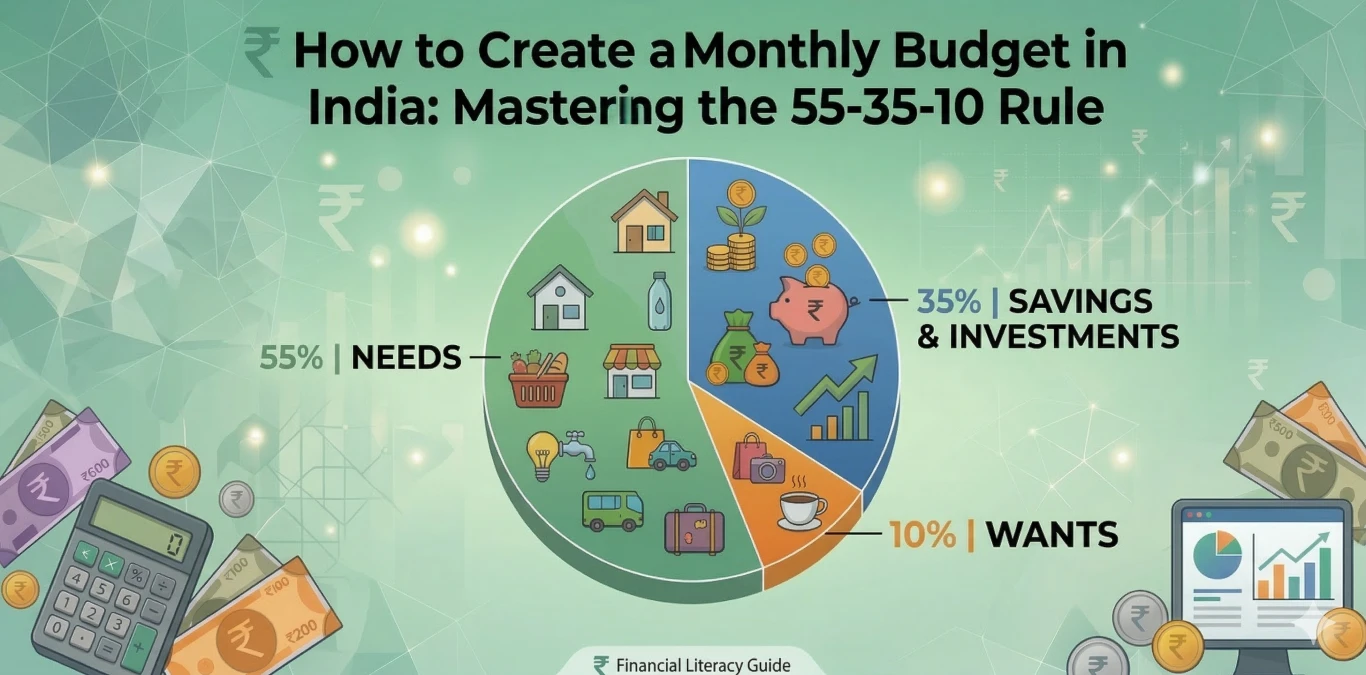

Step 4: Allocating Funds (The Realistic 55-35-10 Indian Approach)

Now, you match your 100% net income to your tracked expenses and future goals.

If you search for budgeting advice online, you may often find the Western “50/30/20 Rule”, which suggests spending 30% on your “wants” and saving only 20%. Do not use this. The Western model relies on state-funded healthcare, free education and social security. In India, we are our own social security. We must independently fund our own retirement, medical emergencies and our children’s higher education.

Therefore, a highly realistic and aggressive wealth-building framework for the Indian context is the 55-35-10 Rule (55% Needs, 35% Savings, 10% Wants). We must also adopt the golden formula of Indian wealth creation: Income – Savings = Expenses.

Here is how you may partition every single rupee you earn:

1. The 35% Bucket: Savings, Investments & Debt (Pay Yourself First) We put this bucket first because of the golden formula. The moment your salary credits, 35% should immediately leave your primary account before you can even look at it.

- Safety First: Building an emergency fund (aiming for 3 to 6 months of basic living expenses) in a liquid mutual fund or a recurring deposit.

- Wealth Creation: SIPs in equity mutual funds. For long-term goals like retirement, many investors look toward large-cap and mid-cap funds to balance stability with growth. You may also consider PPF contributions or physical/digital gold investments.

- Debt Reduction: Paying off high-interest personal loans or credit card debt much faster than the minimum due.

2. The 55% Bucket: Essential Needs Just over half of your net income covers the absolute necessities. We allocate 55% here because inflation, school fees and city rents are high. These are the mandatory expenses you cannot avoid.

- Housing: Rent or Home Loan EMI.

- Daily Bread: Groceries, daily milk and essential household supplies.

- Utilities: Electricity, water, cooking gas and basic internet.

- Obligations: School fees, insurance premiums and basic daily transportation to work, school, etc.

- The Reality Check: If your essential needs are currently consuming 75% or 80% of your income, it is a clear signal that you may need to downsize a specific aspect of your lifestyle or actively seek ways to increase your core income.

3. The 10% Bucket: Wants and Lifestyle You work hard for your money and you absolutely deserve to enjoy it. By keeping your budget at a strict 10%, you eliminate mindless spending but keep the joy of living. This space is your guilt-free zone.

- Dining & Entertainment: Occasional weekend restaurants, Ordering online, movie tickets and OTT subscriptions.

- Shopping: Upgrading your smartphone, buying trendy clothes or pursuing personal hobbies.

- Festivals & Vacations: Saving up for that annual family trip, Diwali gifts or wedding lifafas.

- The Reality Check: If you overspend on dining out, it simply means you must cut back on shopping or movies that month. The strict 10% boundary keeps your lifestyle inflation perfectly in check without making you feel deprived.

Crucial Note: Please remember that while the 55-35-10 rule is a fantastic, highly effective starting point, personal finance is deeply personal. You may need to create your own unique formula based on your specific age, the city you live in, the number of dependants you actively support and most importantly, your actual income level. A young bachelor in Bengaluru may adopt a 40-50-10 rule, while a single-income family in Delhi might need a 65-25-10 rule. Adapt the percentages to serve your reality.

The Reality Check

What if your Needs are already at 80%? What happens if you sit down to calculate your percentages today and you realise your “Essential Needs” are already consuming 80% of your income? First, do not panic and most importantly, do not abandon the budget. This is incredibly common when you are just starting. If your reality right now is an 80-10-10 split (80% Needs, 10% Savings, 10% Wants), then start exactly there. The most important step is to simply start. Use the first month to identify the gaps and where your money is leaking. Do not attempt to force a drastic reduction overnight. Instead, give yourself a realistic 3 to 6-month timeframe to gradually reduce your discretionary expenses or find ways to increase your income, inching your way closer to the ideal 55-35-10 framework. Progress is far more important than immediate perfection.

What happens when your variable income spikes? If you are a freelancer, gig worker, or business owner, you set your baseline budget using your lowest earning month. But what happens when business booms and you bring in significantly more than your baseline? First, congratulations! You worked incredibly hard for that extra revenue, and you absolutely deserve to enjoy the fruits of your labor.

However, using all of that surplus money for discretionary spending can quickly derail your financial stability. Remember, because your income is highly variable, a month of massive surplus might easily be followed by a month of deficit.

To handle this safely and smartly, apply the 90/10 Surplus Rule. Take whatever extra income you earned above your baseline budget and divide it strictly into two parts:

- 10% for the Reward: Add this directly to your “Wants” bucket. Take your family out to celebrate or treat yourself to something nice. Acknowledging and rewarding your hard work is essential to prevent burnout.

- 90% for the Safety Net: Move this immediately into your savings and investments bucket. This massive 90% chunk acts as a powerful financial shock absorber. It guarantees that your family’s essential needs remain fully funded when the inevitable slow business months arrive.

Conclusion: Your First Step Towards Financial Freedom

Creating your very first monthly budget might feel a little overwhelming, but you have just taken the most crucial step toward securing your family’s financial future. By evaluating your income honestly, monitoring your expenditures and implementing the practical 55-35-10 Indian budgeting framework, you are taking control of your wealth.

Remember, your budget is not fixed. The first month you try to follow these percentages, it can be a bit messy. You might forget an annual subscription or a sudden festival might stretch your discretionary spending. That is completely normal! The goal is consistent progress, not immediate perfection.

Your homework is simple: sit down, calculate your family’s exact net income and figure out what your personal 55%, 35% and 10% numbers look like.

What’s Next?

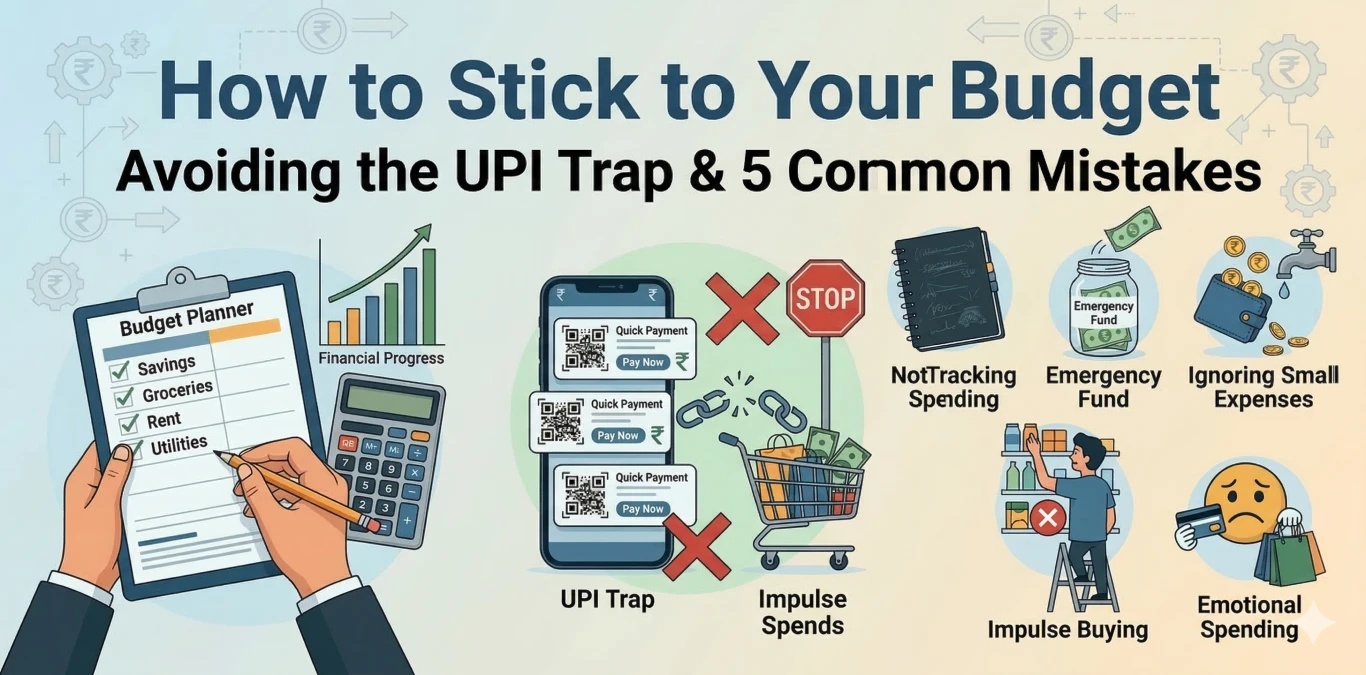

Knowing how much you should spend is only the first half of the battle. The real challenge is knowing how to actually stick to those numbers in the real world.

What happens when you hit your 10% “Wants” limit by the 15th of the month? How do you stop yourself from constantly scanning QR codes and falling into the digital UPI trap? And what are the most common mistakes that cause Indian families to abandon their budgets entirely?

In the next part of this ultimate guide, we dive into powerful, real-world strategies to safeguard your money. We cover the brilliant “Two-Account System,” old-school cash envelope hacks and the best free tools to automate your tracking so you never have to stress about a spreadsheet again.

👉 Ready to master your daily spending? [Click here to read: How to stick to your Budget: Practical Techniques, Avoiding the UPI Trap & 5 Common Mistakes!]

[…] (If you missed that foundational guide, I highly recommend reading it first so you can set up your basic percentages correctly. [Click here to read it here: The Foundation & The 55-35-10 Rule]) […]

[…] on your current cash flow. A highly effective way to structure this in the Indian context is the 55-35-10 rule: allocating 55% of your income to essential needs, 35% to savings and wealth building, and 10% to […]