Have you ever found yourself staring at the ceiling late at night, doing mental math about your upcoming EMIs, the rising cost of groceries, school fees, and wondering how you can ever afford the life you truly desire? If so, you are entirely normal, and you are definitely not alone. The hustle of everyday life in India brings its own unique set of economic pressures. A significant portion of the population struggles with basic financial planning and money consistently ranks as a primary source of anxiety for many middle-class households.

We all have vibrant dreams. You might dream of owning a spacious flat in a good society, traveling with your family across Europe without constantly converting Euros to Rupees in your head, or simply reaching a point where an unexpected medical bill does not induce a state of sheer panic. Dreams are beautiful. However, without a concrete, actionable plan, they remain just dreams floating in the clouds. To pull those aspirations down to earth and make them your reality, you need a solid roadmap. In the world of personal finance, that roadmap is built entirely out of well-constructed, highly realistic financial goals.

Becoming truly wise for life when it comes to your money does not require an advanced degree in finance or a background working at a major brokerage firm. It requires clarity, intentionality and a willingness to be honest about where you stand right now. This comprehensive guide proposes a step-by-step approach to understanding exactly what realistic financial goals are, why they form the absolute foundation of your peace of mind, how to use the proven SMART method to craft them and how to maintain the momentum needed to actually achieve them.

What Are Realistic Financial Goals?

Yes, you read that right: Realistic. We all share the same dream retiring by 30, only to spend the rest of our days on a quiet farmhouse, away from the hustle. It’s a beautiful vision, but let’s bring that dream back to earth for a moment.

To put it simply, a financial goal is a specific objective you propose to achieve with your money within a defined timeframe. The critical keyword we must focus on here is realistic.

A realistic financial goal bridges the gap between your current economic reality and your future desires. It is a target that stretches your discipline but is fundamentally anchored in the reality of your current take-home salary, your essential living expenses and your unique family circumstances. Saying, “I propose to become a crorepati by next month,” is a fantasy (unless you win a lottery, which is not a financial plan). Saying, “I plan to save ₹1 Lakh for a starter emergency fund over the next six months by setting aside ₹16,500 every month,” is a highly realistic, actionable financial goal.

Why Are They So Important?

Living without financial targets is like getting into your car in a chaotic city without a GPS map, just driving around hoping you eventually find your destination. You might get there through sheer luck, but you are likely to waste a tremendous amount of time, fuel and energy in the process. Setting realistic goals does several crucial things for your financial well-being:

1. They provide direction and focus:

When you have a clear target, every single Rupee you earn suddenly has a potential job. It transforms your mindset from wondering, “Where did my salary go at the end of the month?” to declaring, “I am telling my money exactly where it should go.”

2. They change your spending behavior:

It is incredibly difficult to say “no” to an impulse purchase like ordering expensive food online every weekend or buying the latest smartphone on an EMI, when you have no greater purpose for that cash. But when you are actively saving for a down payment on a house, saying “no” to the expensive dinner becomes much easier because you are saying “yes” to your dream home.

3. They create measurable progress:

Targets allow you to look back after three, six or twelve months and see exactly how far you have come. This visible progress acts as the ultimate antidote to financial anxiety.

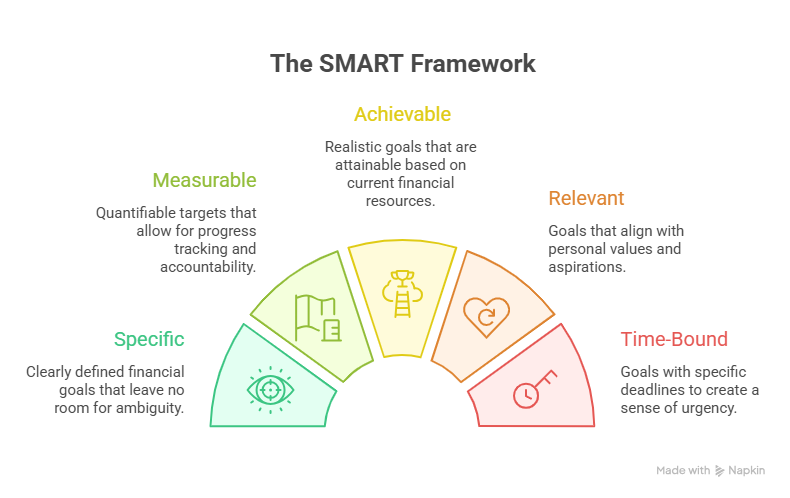

The SMART Criteria: Your Blueprint for Success

If you want your financial goals to transition from vague wishes into actionable plans, you need a robust framework. The most effective framework used by educators, wealth managers and life coaches alike is the SMART criteria. SMART is an acronym that stands for Specific, Measurable, Achievable, Relevant and Time-bound. Let us break down exactly how to apply this to your personal finances.

Specific

Vagueness is the enemy of financial progress. The most common goal people set is simply, “I want to save more money this year.” While the intention is noble, the execution usually fails because the human mind does not know what “more” means. Is it ₹100 or Is it ₹10,00,000?

To make an objective specific, you need to define exactly what you are trying to accomplish. Instead of saying “save money,” a specific target sounds like, “I propose to save enough cash to completely pay off my outstanding personal loan.” Instead of “invest for the future,” a specific objective is, “I plan to open a Public Provident Fund (PPF) account and contribute the maximum limit each year.” Clarity creates action.

Measurable

If you cannot measure it, you cannot manage it. A measurable target includes exact numbers and amounts so you can track your progress along the way. You need to know exactly when you have crossed the finish line.

If your specific aim is to build an emergency fund, the measurable component is the exact Rupee amount. “I propose to save ₹3,00,000 for my emergency fund.” Once you have that number, you can break it down into bite-sized, measurable milestones. If you want to achieve this in ten months, you can measure your progress by checking if you are saving exactly ₹30,000 each month. Tracking your progress whether in a simple diary, an Excel spreadsheet or a budgeting app provides a powerful psychological boost that keeps you moving forward.

Achievable

This is where the word “realistic” takes center stage. Your targets must be physically and mathematically possible based on your current cash flow. A highly effective way to structure this in the Indian context is the 55-35-10 rule: allocating 55% of your income to essential needs, 35% to savings and wealth building, and 10% to wants.

If your in-hand salary is ₹60,000 a month, your 35% savings capacity is ₹21,000. Setting a goal to save ₹30,000 a month is mathematically impossible without drastically increasing your income or shifting to a much cheaper location. Setting a target that is entirely out of reach does not motivate you; it only sets you up for inevitable failure, “frugal fatigue,” and the likelihood that you will abandon your plan entirely. An achievable goal in this scenario would be utilizing your ₹21,000 savings capacity strategically, while keeping your 10% “fun money” intact so you don’t burn out.

Relevant

Does this goal actually matter to you? In Indian society, it is incredibly easy to adopt the financial expectations of your relatives, your neighbors, or societal norms. If a goal does not align with your deeply held personal values, you will quickly lose the emotional resilience needed to avoid expensive weekend food deliveries or massive online festival sales.

For example, you might feel intense societal pressure to take out a massive personal loan to host a lavish, 500-guest wedding, or feel obligated to buy gold during Dhanteras simply because everyone else is doing it. But if you personally value travel, quiet experiences, and a stress-free life far more than a grand display of wealth, paying that heavy loan EMI every month will feel like a miserable chore. Ensure your goals resonate with the life you actually want to build.

Time-Bound

A goal without a deadline is merely a suggestion. Giving yourself a specific timeframe creates a sense of healthy urgency. It forces you to prioritize your target today, rather than putting it off until some imaginary “tomorrow.”

“I want to save ₹5 Lakhs for a home renovation” is a good start, but it lacks urgency. “I propose to save ₹5 Lakhs for a home renovation before Diwali next year” is a SMART goal. The deadline forces you to do the math: if you have exactly 12 months, you know you need to set aside about ₹41,600 per month. The deadline dictates your monthly behavior and holds you accountable.

Types of Financial Goals: Breaking It Down

To build a comprehensive financial roadmap, you need to look at your life in phases. Financial experts generally categorize goals into three distinct timelines: short-term, medium-term and long-term. Balancing your focus across all three ensures you stay protected today while still actively preparing for tomorrow.

Short-Term Financial Goals (0 to 1 Year)

Short-term goals form the absolute foundation of your financial house. They are usually focused on creating stability, providing immediate security and clearing away pressing roadblocks.

Building a Starter Emergency Fund:

Life is entirely unpredictable. Two-wheelers break down, appliances need fixing, and unexpected medical situations arise. Your very first short-term goal should be creating a financial shock absorber.

Let’s put this through the SMART engine: If your Specific and Measurable goal is to save ₹50,000, and your Time-bound deadline is six months, the math dictates you must save exactly ₹8,333 a month. Seeing that exact number forces you to check if it’s Achievable. If your budget only allows for ₹5,000 of savings right now, you don’t abandon the goal—you simply stretch the timeline to ten months. This visible math acts as a buffer between you and the potholes of life, ensuring that a minor emergency does not force you into swiping a credit card.

Paying Off High-Interest Debt:

Credit card debt and personal loans act as financial emergencies. With credit card interest rates often hovering between 40% and 48% annually in India, carrying a balance essentially destroys any wealth you might build elsewhere. A crucial short-term goal is to list your debts, pick a strategy (like paying the smallest balance first for psychological wins or tackling the highest interest rate first for mathematical efficiency), and aggressively clear them.

Saving for Annual Expenses:

We all have those expenses that pop up once a year life insurance premiums, school admission fees or festive shopping. A great short-term goal is to calculate the total annual cost of these items, divide by 12 and save that amount monthly in a recurring deposit (RD) or a dedicated savings account. When the festival season arrives, the money is already waiting.

Medium-Term Financial Goals (1 to 5 Years)

Once your immediate foundation is stable, you can start looking slightly further down the road. Medium-term goals are usually larger purchases or significant life transitions that require a few years of steady, disciplined saving.

Building a Fully Funded Emergency Reserve:

While a starter fund protects you from minor inconveniences, a fully funded emergency reserve protects you from major life events, such as a sudden job transition or a prolonged health issue. A standard medium-term goal involves expanding your starter fund to cover three to six months’ worth of essential living expenses.

Saving for a Down Payment:

If purchasing a home is a relevant aspiration for you, accumulating a down payment is a classic medium-term objective. Because you might need this money in a relatively short timeframe, it is generally best kept out of volatile equity markets and placed in safer, interest-bearing instruments like Fixed Deposits (FDs) or conservative debt funds.

Cash-Flowing a Vehicle Upgrade:

Car loans can act as a massive drain on your monthly cash flow. A fantastic medium-term goal is to save enough money to buy your next vehicle with a very heavy down payment, ensuring that any remaining EMI is incredibly small and manageable.

Long-Term Financial Goals (5+ Years)

Long-term goals represent the marathon of personal finance. They require you to project yourself far into the future and use the magic of compound interest to your absolute advantage.

Retirement Planning:

Whether you are in your 20s or your 40s, building a retirement corpus must be on your radar. The objective here is to accumulate enough invested capital so that the returns generated can eventually replace your working salary. Because this timeline is long, you can afford to invest in equities (often through diversified mutual funds via SIPs) to comfortably beat inflation over time.

Children’s Education:

The cost of higher education is rising rapidly. The earlier you start, the less painful the process becomes. For example, suppose you are planning for your three-year-old daughter Srisha’s higher education. Paying for her college might feel like it is decades away.

However, by applying the SMART framework—setting a Measurable target of a specific corpus and a Time-bound horizon of exactly 15 years—you realize you don’t need all the money today; you just need to let compounding do the heavy lifting. Starting a dedicated Systematic Investment Plan (SIP) right now means that even a small, consistent monthly contribution grows into a substantial sum by the time Srisha is ready to fill out university applications.

Paying Off the Home Loan Early:

Imagine what your monthly cash flow might look like if you did not have a massive home loan EMI leaving your account on the 5th of every month. Making extra principal payments on your home loan to become debt-free years ahead of schedule is a powerful long-term goal that drastically reduces your financial risk and increases your freedom.

How to Stay Motivated and Tracking Progress

Starting a new goal feels great, and the first week is always the most exciting. But when you’re saving money for something far in the future, it’s easy to lose that spark. You eventually hit a “boring middle” phase where the early excitement has worn off, but you’re still a long way from reaching your target. Here are practical ways to maintain your momentum.

1. Automate Everything:

Willpower remains a finite resource. If you have to consciously choose to log into your banking app and transfer money to your savings account every single payday, eventually, you might forget or you might justify spending it instead. Remove human error from the equation. Set up automatic bank mandates (NACH) so that the moment your salary hits your account, a portion is instantly routed to your SIPs, RDs.

2. Keep It Simple:

It is easy to get distracted by complex Trading charts, the thrill of day trading or the latest hot stock tip from a WhatsApp group. However, genuine wealth creation starts with simple, consistent goal setting. Focus on executing the basics before you attempt to innovate or complicate your portfolio.

3. Make It Visual:

Human beings thrive on seeing visual progress. If you propose to pay off ₹2,00,000 in debt, create a visual tracker. Draw a thermometer on a piece of paper, stick it to your refrigerator and color it in for every ₹10,000 you clear. Seeing the marker rise toward the top serves as a powerful daily reminder of what you are working toward.

4. Celebrate the Milestones:

You cannot sprint a marathon; you must pace yourself carefully. If your goal involves saving ₹10 Lakhs for a house down payment, do not wait until you hit the final amount to feel good about it. Celebrate every ₹2 Lakh milestone. Treat your family to a nice (but budgeted) dinner or enjoy a simple, joyful activity together. Acknowledging your hard work prevents you from experiencing “frugal fatigue.”

5. Forgive Yourself for Slip-Ups:

You are human. There are bound to be months where the budget completely falls apart, where an emergency wipes out your savings or where you simply give in to a moment of weakness and overspend during a festival sale. The key to long-term success lies in resilience. Do not let one bad week derail a five-year plan. Acknowledge the mistake, figure out what triggered it and simply start again the next day with renewed focus.

Common Pitfalls to Avoid

As you embark on this journey, be highly mindful of the common traps that derail many well-intentioned planners.

Trying to Do Everything at Once

The quickest way to fail at goal setting is trying to tackle too many things simultaneously. You cannot aggressively pay off a personal loan, save for a massive down payment, fully fund your retirement and plan a lavish international vacation all at the exact same time on an average income. Doing so spreads your money too thin, resulting in negligible progress across the board. Focus provides power. Pick one or two primary financial goals, attack them with intensity until they are complete and then move down your list.

Ignoring the Emergency Fund

Many people get so excited about investing in the stock market or clearing debt that they completely skip building an emergency fund. This acts as a critical error. Without an emergency fund, the first time you face a medical crisis or an urgent repair, you are forced to use credit cards, sending you straight back into the debt trap. The emergency fund acts as your defensive line; you must build it before you go on the offensive.

Succumbing to Lifestyle Inflation

As you progress in your career, your income naturally increases. The most dangerous trap is “lifestyle inflation,” where your spending rises perfectly in tandem with your salary hikes. For example, you get a ₹1,50,000 yearly appraisal and suddenly you upgrade to a bigger car that costs exactly ₹1,50,000 more in EMIs. To truly accelerate toward your financial targets, you must fight lifestyle inflation. When you start making more money, try not to spend more. Instead of buying extra things, put that new money into your savings or investments to grow your wealth.

Being Too Rigid

While discipline remains necessary, an overly rigid budget often feels like a financial prison. If you stop doing everything that makes you happy, like enjoying a cup of coffee outside, going to the movies or buying a book, you might get really tired and end up spending a lot of money just to feel better. A realistic budget must include a specific line item for “fun money.” Give yourself permission to spend a small, set amount each month completely guilt-free.

Conclusion

Mastering your personal finances is not a one-time event; it is a lifelong process of learning, adjusting and growing. Setting realistic financial goals serves as the most powerful step you can take toward taking absolute control of your future. By defining what you truly desire, running those aspirations through the SMART framework and breaking them down into short, medium and long-term actionable steps, you strip away the anxiety that so often surrounds money.

Remember to be patient with yourself throughout this journey. Wealth building is a slow, highly methodical process. By staying focused, avoiding the dangerous trap of comparison and consistently executing your plan month after month, you can successfully achieve your goals. More importantly, you can build a solid foundation of financial peace that supports you and your family for decades to come. Take out a pen and paper today, look honestly at your numbers, and take that crucial first step toward true financial independence.