Retirement planning in India used to be straightforward. You worked for a single employer for three decades, received a guaranteed pension and relied on a robust joint-family system for physical and emotional support.

Today, that landscape has fundamentally shifted. The traditional joint family is increasingly giving way to nuclear setups and structured corporate pensions are largely a thing of the past for the private sector. The rising healthcare costs and inflation constantly eroding fixed-income returns, building a self-reliant retirement corpus is an absolute necessity.

Compounding this challenge is the rising popularity of the FIRE (Financial Independence, Retire Early) movement among younger generations, which requires compressed timelines for wealth accumulation. Whether your goal is to retire early or to transition comfortably at 60, retirement planning is not a one-time calculation. It is an evolving strategy that must adapt as you move through different stages of life.

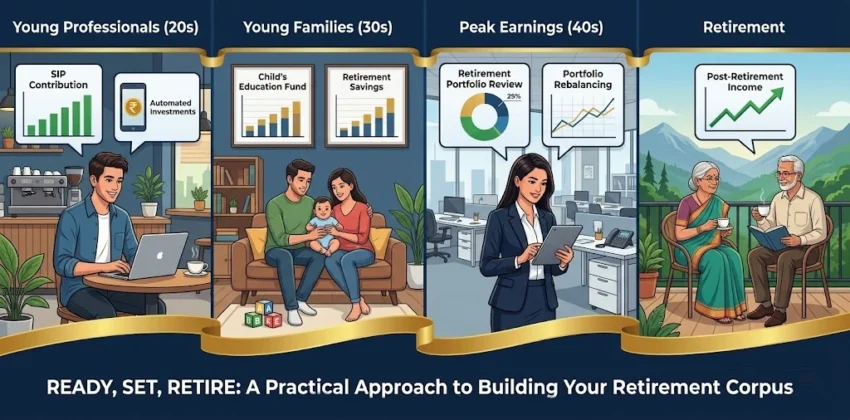

1. The Foundation Stage: Young Professionals (Ages 21–29)

As a young professional entering the workforce, retirement feels incredibly distant, perhaps 35 to 40 years away. When you are dealing with entry-level salaries, rent, and the desire to establish a lifestyle, saving for the year 2060 feels like a low priority.

This life stage holds a financial superpower that disappears with age that is time. Thanks to compounding, a small amount invested in your 20s can grow significantly larger than double that amount invested in your 30s.

The Financial Realities

At this stage, your income is typically at its lowest point, but your financial liabilities (dependents, home loans) are also minimal. The primary goal here is habit formation and capital growth.

Actionable Strategies

- Automate via Equity SIPs: Because retirement is decades away, your investment horizon can withstand short-term market volatility. Investing through Systematic Investment Plans (SIPs) in diversified equity mutual funds is highly effective here. Historically, Indian equities have outpaced long-term retail inflation, making them well-suited for wealth accumulation.

- Maximise the Employee Provident Fund (EPF): Treat your mandatory EPF contribution as the debt or fixed-income portion of your retirement portfolio. If your employer offers a Voluntary Provident Fund (VPF), consider opting in to increase your fixed-income allocation with tax-free or tax-exempt returns under current laws.

- Build a Basic Safety Net: Before investing heavily, establish an emergency fund equal to three to six months of your living expenses in a liquid savings account or liquid fund. Additionally, buy independent health insurance; relying solely on corporate health cover is risky if you change jobs or face unemployment.

Case Study: The Cost of Waiting

Consider Rohan, who starts investing ₹5,000 every month in an equity mutual fund at age 25. Assuming a conservative long-term average annual return of 12%, by the time he reaches age 60, his corpus will grow to approximately ₹3.24 crore.

Now look at Priya, who waits until age 35 to start investing the exact same amount under the same conditions. By age 60, her corpus will be worth roughly ₹95 lakh. By delaying her start by 10 years, Priya ends up with less than a third of Rohan’s final amount, despite only missing 10 years of contributions.

2. The Accumulation & Balancing Stage: Young Families (Ages 30–39)

In your 30s, financial complexity intensifies. This is the stage where major life milestones intersect: marriage, buying a home, and raising children.

The deeper tension here is the “sandwich” squeeze. You are suddenly balancing immediate, high-priority costs like school fees or home loan EMIs, against a distant retirement goal. It is common for individuals at this stage to pause their retirement savings to fund short-term family needs, which can significantly disrupt long-term compounding.

The Financial Realities

Your income is rising but your expenses are rising just as fast, if not faster. The goal shifts from pure growth to structured allocation and risk management.

Actionable Strategies

- Adopt the “Step-Up” Approach: As your income grows through annual increments or promotions, increase your retirement SIPs proportionally. If your salary increases by 10% this year, try increasing your monthly investment amount by 5% to 10%. This prevents “lifestyle creep” from consuming your surplus cash.

- Utilize the National Pension System (NPS): The NPS is a highly effective, low-cost tool for this life stage. It offers low fund management fees and provides additional tax benefits under Section 80CCD(1B) of the Income Tax Act. Opt for the “Active Choice” where you can maintain up to 75% equity exposure in your early 30s, gradually tapering down as you age.

- Separate Retirement from Child Education Goals: A common pitfall in India is using retirement funds to pay for higher education. Remember: children can get education loans; you cannot get a retirement loan. Keep these portfolios completely separate.

| Goal / Priority | Suggested Investment Vehicle | Ideal Asset Allocation |

| Retirement Fund | Equity Mutual Funds + NPS + EPF | 60-70% Equity / 30-40% Debt |

| Child’s Education (10+ years away) | Diversified Equity & Aggressive Hybrid Funds | 50% Equity / 50% Debt |

| Home Down Payment (Short-term) | Recurring Deposits / Arbitrage Funds | 100% Debt / Low-risk |

3. The Peak Earnings Stage: Mid-Career Professionals (Ages 40–49)

By your 40s, you are likely entering your peak earning years. However, this is also the period of peak expenses. Children are entering high school, elderly parents may require medical care, and your own lifestyle costs have expanded.

The psychological trap of this stage is complacency. Because your bank balance looks healthier than it did in your 20s or 30s, it is easy to assume you are on track without doing the actual math.

The Financial Realities

This is the critical decade where you must bridge any gaps in your retirement target. You have less time to recover from major market downturns, meaning your asset allocation requires a thoughtful look.

Actionable Strategies

- Run a Retirement Audit: Calculate your exact target corpus based on your current lifestyle expenses, projected into the future using an estimated inflation rate (historically around 6% to 7% in India for lifestyle and higher for healthcare). Assess your current investments against this target.

- De-risk Gradually via Rebalancing: If your portfolio has drifted heavily into equities due to a bull market, actively rebalance it back to your target asset allocation. Move excess gains into safer debt instruments like Public Provident Fund (PPF), debt mutual funds, or corporate bonds to protect your capital.

- Upgrade Medical Insurance Independently: Health risks increase noticeably in your 40s. Do not depend entirely on your employer’s health insurance. Secure a comprehensive family floater health insurance policy with a substantial super top-up plan to ensure a medical emergency does not wipe out your retirement savings.

4. The Consolidation Stage: Near-Retirees (Ages 50–60)

In your 50s, the countdown begins. The primary focus shifts from wealth accumulation to wealth preservation. Your primary enemy at this stage is no longer just inflation but sequence-of-returns risk—the risk that a major stock market crash right before you retire could permanently shrink your nest egg before you even begin drawing from it.

The Financial Realities

Liabilities like home loans are ideally winding down, and children may be starting their own careers, freeing up cash flow. However, your time horizon to recover from market shocks is very short.

Actionable Strategies

- The Bucket Strategy Construction: Divide your accumulated corpus into three distinct “buckets” to manage risk and provide peace of mind:

- Immediate Bucket (Years 1–5): Keep 5 years of living expenses in ultra-safe, liquid instruments like Senior Citizens Savings Scheme (SCSS), banking fixed deposits, and liquid funds.

- Medium-Term Bucket (Years 6–10): Invest this portion in conservative hybrid funds or high-quality corporate debt to outpace inflation while keeping volatility low.

- Growth Bucket (Years 11+): Leave the remaining portion in diversified equity funds so that your corpus continues to grow and combat long-term inflation over a 20-to-30-year retirement.

- Clear All High-Interest Debt: Make it a priority to enter retirement completely debt-free. Use maturity proceeds from old insurance policies or year-end bonuses to clear outstanding home loans or personal loans.

- Plan for Post-Retirement Cash Flows: Start mapping out exactly how your monthly “paycheck” will look. Familiarize yourself with Systematic Withdrawal Plans (SWPs) in mutual funds, which can provide regular income in a highly tax-efficient manner compared to traditional annuity products or standard fixed deposits.

Summary of Actionable Steps across Life Stages

To keep your planning focused, here is a consolidated checklist of immediate actions based on where you are today:

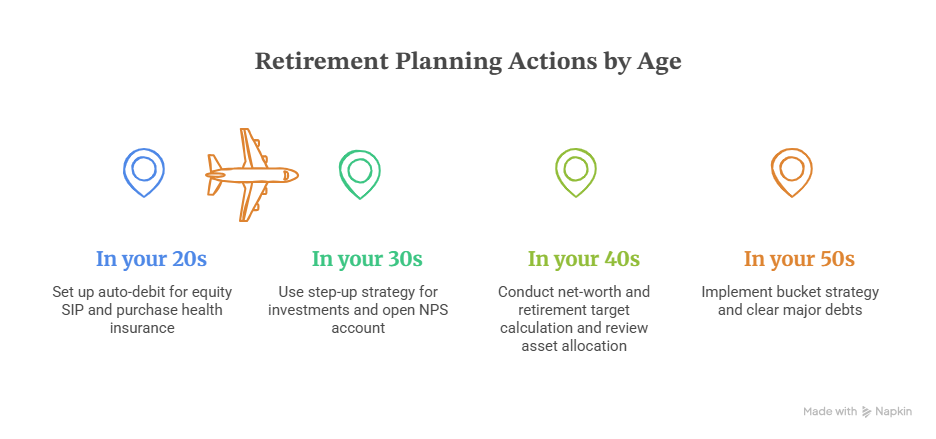

- In your 20s: Set up an auto-debit for at least one equity SIP the day after your salary hits your account. Purchase an independent health insurance policy immediately.

- In your 30s: Use the step-up strategy to increase your investment amounts with every appraisal. Open an NPS account to claim additional tax benefits and lock away long-term savings.

- In your 40s: Conduct a comprehensive net-worth and retirement target calculation. Review your asset allocation to ensure you are not taking unintended risks.

- In your 50s: Implement the bucket strategy to protect the next five years of your living expenses from market swings. Ensure all major debts are cleared before your final working day.

Conclusion

Thinking about retirement can naturally provoke anxiety. It requires confronting a future where you no longer draw a regular salary while facing unpredictable health and economic conditions. Feeling overwhelmed by the sheer scale of the numbers required is completely normal.

However, the antidote to financial anxiety is deliberate, structured action. Retirement planning is not about starving your present self to feed your future self; it is about finding a balance that honors both. You do not need to perfect your entire strategy today. Pick one small, manageable step appropriate for your current life stage—whether that is setting up a ₹2,000 SIP, checking your current EPF balance, or reviewing your health cover. By taking control of the variables you can influence today, you build a foundation for a dignified, independent tomorrow.