Imagine this: It’s the middle of the night, and a family member suddenly falls seriously ill. Or perhaps it is a regular Monday morning, and you are called into a meeting only to realise your company is downsizing and your role has been eliminated. In life, the unexpected is the only true certainty. When these moments strike, they bring an immense emotional toll. The last thing you want to worry about is whether you can afford to pay for the solution.

This is where a robust emergency fund steps in. Think of it as a financial shock absorber. You set aside this dedicated pool of money strictly to cover unexpected, urgent life events.

In India, building a self-reliant safety net is more critical than ever. Unlike many Western countries, India doesn’t have a widespread, state-sponsored social security net for private-sector employees or self-employed individuals. If you lose your job or face an unexpected medical crisis, the financial burden rests squarely on your shoulders.

Establishing a powerful financial safety net is not an overnight task, but it is one of the most liberating steps you will ever take for your long-term peace of mind. Let’s dive into a comprehensive, step-by-step roadmap to building an emergency fund tailored directly to the Indian economic landscape.

Understanding the “Why”: The Crucial Need for a Safety Net in India

Living and working in India exposes your finances to unique, fast-moving variables. To understand why a dedicated cash cushion is non-negotiable, consider the most common financial shocks an Indian household faces:

- Skyrocketing Healthcare Costs: While medical science has advanced rapidly in India, private healthcare costs are outpacing general inflation. Even if you have corporate health insurance, hidden charges, non-medical expenses, or co-payments can leave a massive hole in your pocket during a medical emergency.

- Job Volatility and Sectoral Shifts: From tech layoffs in major IT hubs like Bengaluru and Hyderabad to shifting economic tides affecting startups and manufacturing, employment stability is no longer guaranteed. Finding a comparable job in a competitive market can take anywhere from three to nine months.

- The Debt Trap: When crisis hits and cash isn’t available, many people resort to quick personal loans or swipe their credit cards. In India, credit card revolving interest rates can soar as high as 36% to 42% per annum. Once you enter this high-interest debt cycle, climbing out becomes an uphill battle that can derail your future financial goals, like buying a home or planning for retirement.

- Family Responsibilities: Indian families often support parents, siblings, or relatives during difficult times. Sudden travel, medical support, or financial assistance may become necessary without warning.

- Unexpected Repairs: Vehicle breakdowns, appliance replacements, plumbing problems, or urgent house repairs can arise anytime and disrupt monthly budgets.

- Natural Disasters and Economic Shocks: Floods, heatwaves, crop failure, pandemics, or economic slowdowns can affect both urban and rural households.

Ultimately, an emergency fund gives you time. It buys you the grace period to make calm, rational decisions instead of desperate, panic-driven ones.

Step 1: Calculate Your Target Emergency Fund Size

Before you save your first rupee, you need a precise target. A vague goal like “I want to save a lot of money” usually leads to inconsistent savings. You need a hard number backed by data.

1. Identify Your Monthly Essential Expenses

An emergency fund is designed to keep your life afloat, not to fund luxury lifestyle choices. Track your bank and credit card statements for the last three months and separate your spending into two distinct buckets:

| Essential Expenses (Needs) | Discretionary Expenses (Wants) |

| Rent or Home Loan EMI | Dining out and ordering via food delivery apps |

| Groceries, milk, and vegetables | OTT subscriptions |

| Utilities (Electricity, water, Wi-Fi, mobile recharges) | Weekend shopping or movie outings |

| School/College fees for children | Vacations and leisure travel |

| Transport costs (Petrol, metro fare, cab expenses) | Upgrading gadgets prematurely |

| Insurance premiums (Health, Life, Car) | Gym memberships or hobby classes |

| Mandatory loan EMIs (Car loan, education loan) |

Your emergency fund calculation must focus strictly on the Essential Expenses column.

2. Decide on the Number of Months to Cover

The traditional rule of thumb is to save 3 to 6 months of essential expenses. However, depending on your professional and personal circumstances, you may need to scale this up:

- Aim for 3 to 6 months if: You have a stable corporate job, multiple earning members in the household and healthy medical insurance coverage.

- Aim for 6 to 9+ months if: If your income fluctuates as a freelancer, independent contractor, or small business owner, you should choose a larger fund. You should also opt for a bigger safety net if you are your family’s single breadwinner or support aging parents with chronic health conditions.

3. Apply the Formula

Once you have your numbers, use this direct formula:

Let’s look at a practical scenario of a typical urban Indian household:

Scenario: Rajesh and Priya live in Mumbai with one child. They map out their baseline monthly survival costs:

- Home Loan EMI: ₹35,000

- Groceries & Vegetables: ₹12,000

- Electricity, Wi-Fi & Mobile: ₹4,500

- School Fees (Pro-rated monthly): ₹5,000

- Fuel & Maintenance (Car): ₹6,000

- Term & Health Insurance Policy (Pro-rated monthly): ₹2,500

Total Monthly Essential Expenses: ₹65,000

Because Rajesh works in a volatile startup environment, they decide a 6-month cushion is safest.

Their target emergency fund size is ₹3.9 Lakhs.

Step 2: Where to Park Your Emergency Fund

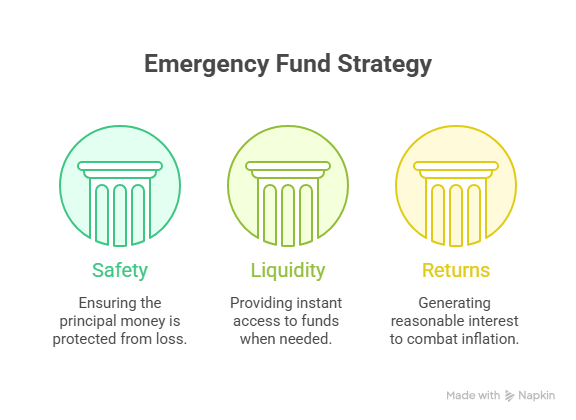

An emergency fund requires a completely different strategy than long-term investing. When picking a financial home for this money, you must prioritize three pillars in this exact order: Safety, Liquidity and Returns.

Because no single financial instrument fulfils all three perfectly, the smartest approach for an Indian saver is to split the fund across a few different avenues.

1. Regular Savings Bank Account (For Immediate Cash)

Keep roughly 10% to 20% of your emergency fund here. If you need cash at 2:00 AM on a Sunday for a hospital payment or an immediate pharmacy run, your debit card gives you the fastest access.

- Pros: Instant access via ATMs, UPI and net banking.

- Cons: Low interest rates (typically 3% to 4%) which fail to beat India’s inflation rate, meaning your money gradually loses purchasing power if left here long-term.

2. Sweep-in / Flexi Fixed Deposits (FDs)

This is an exceptional tool offered by almost all major Indian banks. A sweep-in FD links your regular savings account to a fixed deposit. When your savings account balance crosses a certain threshold, the excess money automatically “sweeps” into an FD earning higher interest (often 6% to 7.5%). If you write a cheque or make a UPI payment that exceeds your savings balance, the FD automatically breaks in exact fractions to cover the deficit without a penalty.

- Pros: Earns FD-level returns while remaining entirely liquid.

- Cons: Yields are fully taxable as per your income tax slab.

3. Liquid Mutual Funds

Liquid funds are debt mutual funds that invest in highly secure, short-term market instruments like government securities and treasury bills that mature within 91 days. They are heavily regulated by the Securities and Exchange Board of India (SEBI) to minimize risk.

- Pros: Better yield potential than a standard savings account. Many top asset management companies (AMCs) offer an “instant redemption” feature, allowing you to transfer up to ₹50,000 or 90% of your fund value to your bank account instantly via an app, 24/7. The remaining balance hits your account within one business day (T+1).

- Cons: Not completely risk-free (though extremely low-risk) and returns fluctuate slightly based on prevailing interest rates.

What to Absolutely Avoid

Never place your emergency fund into volatile assets like direct stocks, equity mutual funds, crypto or long-term real estate. If the stock market crashes by 20% on the exact week you lose your job, you would be forced to book a massive loss just to pay your bills.

Step 3: Actionable Strategies to Build the Fund

If your calculated target looks intimidating, do not lose heart. You don’t have to fund it all in one go. The secret lies in systematic progression.

- Automate to “Pay Yourself First”: Do not save what is left after spending; spend what is left after saving. Set up an automated standing instruction in your salary account for the day after your payday. Let ₹5,000, ₹10,000 or whatever fits your budget move directly into your dedicated emergency container automatically.

- Route Your Windfalls: India has a rich culture of festive bonuses (like Diwali bonuses), performance incentives and tax refunds. Whenever you receive a financial windfall, commit to allocating at least 50% of it directly into your emergency fund until the target is met.

- Audit Your Subscriptions and Convenience Fees: Small leakages sink great ships. Review your credit card statements for automatic monthly payments. Are you paying for three different streaming apps when you only watch one? Are you spending thousands every week on hyper-convenience delivery apps when a quick walk to the local kirana store would cost far less? Redirect these small savings straight into your emergency pool.

- Gamify Your Milestones: Break your macro goal into micro-milestones. Celebrate when you hit Month 1 of survival expenses, then Month 2 and so forth. Watching the container fill up creates a psychological momentum that makes saving addictive.

Step 4: The Golden Rules of Maintenance

Once you build your emergency fund, you will find that leaving it alone is the hardest part. You must set strict boundaries to ensure the fund remains intact for genuine crises.

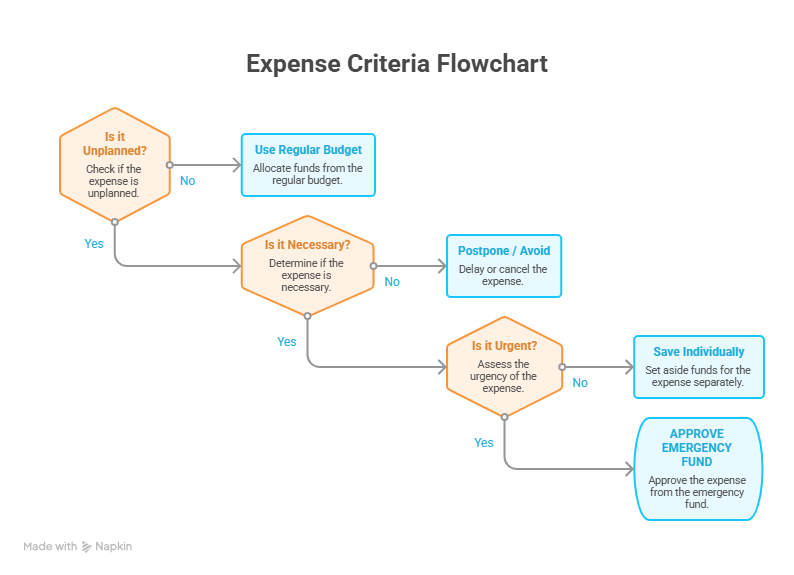

Defining a True Emergency

Before tapping into your fund, put the expense through a simple, objective checklist:

- Is it unexpected? (A medical bill is unexpected; a planned car service or a friend’s wedding gift is not).

- Is it absolutely necessary? (Fixing a leaking roof during the monsoon is necessary; upgrading to the latest smartphone because your screen has a tiny scratch is not).

- Is it urgent? (Does it need to be paid right now to avoid severe legal, professional, or medical consequences?)

The Replenishment Rule

If a real emergency forces you to use a portion of your fund, your financial priorities must temporarily pivot. Stop all discretionary investing (like extra mutual fund SIPs targeted for wealth creation) and route those cash flows back into your emergency account until it returns to its full, baseline strength.

Account for Inflation Annually

As the cost of living rises in India, your baseline monthly survival number will expand over time. Review your calculator once every year—ideally during your annual appraisal or at the start of the financial year in April. Adjust the total target up by a realistic margin to match your current lifestyle inflation.

Conclusion

Building a robust emergency fund requires patience, discipline, and a willingness to trade temporary gratification for long-term protection.

The greatest return on investment an emergency fund delivers cannot be measured by an interest rate or a percentage yield on a spreadsheet. Its true value is measured in the sound sleep you experience every night, knowing that no matter what life throws at your family, you have the financial armour to withstand the storm.

Take your first step today. Track your essential expenses tonight, calculate your number and set up your automated savings transfer. Your future self will thank you for it.