Imagine you are applying for a home loan. To prove your financial eligibility, you spend a hectic Saturday logging into three different banking portals, downloading six-month PDF statements, scanning physical copies of your mutual fund statements, and tracking down your latest EPF slip. You wrap these up in an email or, worse, send them over WhatsApp to a loan agent.

Within days, you find yourself vulnerable to a barrage of spam calls offering unwanted credit cards or insurance policies. Your private financial history is now floating across random hard drives and chat histories.

This chaotic, insecure process has been the reality of personal finance in India for decades. However, a major digital shift is quietly fixing this mess. Just as the Unified Payments Interface (UPI) completely transformed how we send money, India’s Account Aggregator (AA) Framework is revolutionising how we share financial information.

Regulated by the Reserve Bank of India (RBI), the AA network acts as a secure, digital pipeline.1 It allows you to share your financial data instantly and safely between institutions, putting you firmly in control of your own information.

1. The Mechanics: How Account Aggregator Ecosystem Works

To understand the Account Aggregator system, it helps to understand its place in India’s technology landscape. The AA framework serves as the data exchange layer of our Digital Public Infrastructure (DPI) perfectly complementing Aadhaar (which proves who you are) and UPI (which handles how you pay).2

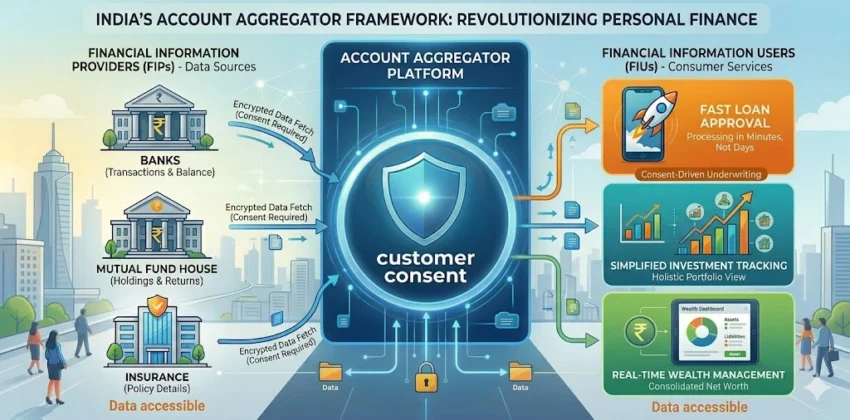

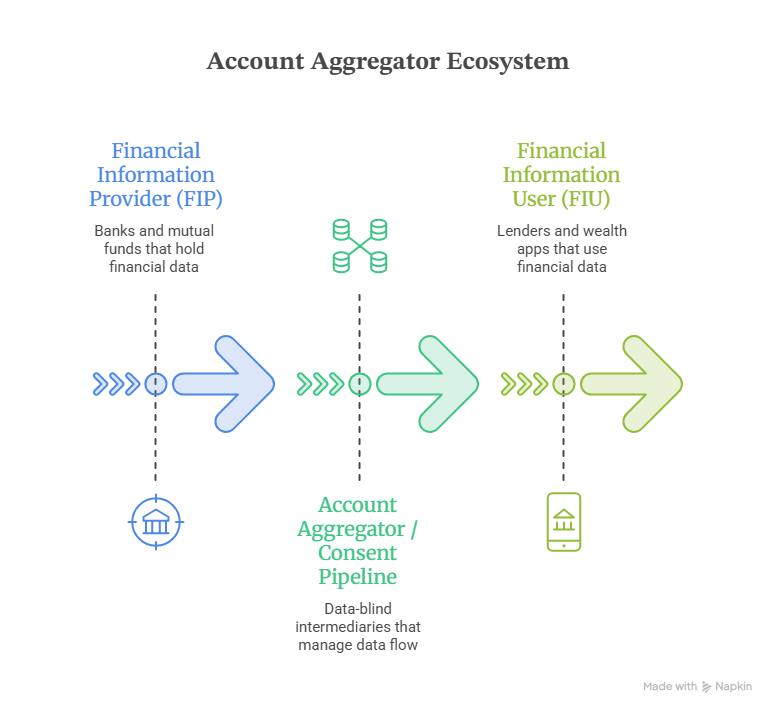

An Account Aggregator (AA) operates as a specialized, RBI-regulated entity designed to give individuals complete ownership over their financial records. The framework functions purely on explicit user permission; it securely moves data from one financial institution to another only when you authorize it. Signing up for an AA is entirely optional, and the central bank has currently authorized seventeen companies to provide this digital consent management service. 3

At its heart, an Account Aggregator is a consent manager. It is an app or platform that acts as a middleman between where your financial data lives and where it needs to go. Crucially, an Account Aggregator is data-blind. It cannot see, read, or store your data; its only job is to securely transfer it based on your explicit instructions.

To make sense of the ecosystem, let’s break it down into three key pillars:

- Financial Information Providers (FIPs): These are the institutions that currently hold your financial data. Examples include your salary bank account, your mutual fund depository (like CAMS or NSDL), your insurance company, or the Income Tax Department.

- Financial Information Users (FIUs): These are the regulated entities that need to view your financial history to provide you with a service. This could be a bank assessing you for a vehicle loan, a personal finance app helping you track your wealth, or a robo-advisor planning your retirement.

- Account Aggregators (AAs): Regulated as specialised Non-Banking Financial Companies (NBFC-AAs) by the RBI, these platforms manage the pipeline. They receive a data request from an FIU, display it transparently on your smartphone, and ask for your approval. If you agree, they fetch the data from the FIP and deliver it to the FIU in an encrypted format.

A Real-World Example

Suppose you use a modern Personal Finance Management (PFM) app to track your net worth. In the past, you would have to manually input your savings balances or upload mutual fund statements every month.

With the AA framework, the PFM app (the FIU) sends a request to your Account Aggregator. You open your AA app, see the request, and tap “Approve.”

Instantly, your bank and mutual fund house (the FIPs) securely send your balance and portfolio data to the app. Your dashboard updates in real time, without you ever sharing a single password or filling out a spreadsheet.

2. Practical Benefits: Revolutionising Loans and Wealth Management

The AA framework is not just a backend upgrade for banks; it delivers tangible, everyday benefits to your personal finances.

A. Securing Loans Instantly and Fairly

When you apply for a personal or business loan, lenders evaluate your creditworthiness by analyzing your cash flow. Traditionally, this meant gathering physical paperwork or uploading PDFs. This approach creates an administrative bottleneck and slows down approvals.

With AA, the entire underwriting process becomes digital and frictionless:

- Speed: Lenders can verify your income and banking transactions in minutes rather than days. This enables true “sachet loans”—small, short-term credit products tailored for emergencies or minor business expenses.

- Fairer Assessment: If you are a freelancer, a small business owner, or someone without a traditional credit score (CIBIL), traditional banks might struggle to evaluate you. By securely sharing your real-time cash inflows and outflows via AA, you provide clear proof of your ability to repay, opening doors to formal institutional credit.

B. Consolidated Wealth and Mutual Fund Tracking

Most Indians have their savings and investments scattered across multiple platforms—a Public Provident Fund (PPF) account with a state bank, fixed deposits with another commercial bank, and mutual funds managed via separate distributors. Getting a single, accurate view of your net worth is remarkably difficult.

The AA ecosystem brings this together. By linking your investment repositories, you can view your entire financial life on a single dashboard.

This single-view capability allows automated financial advisors to analyze your actual asset allocation, spot if you are holding too much idle cash, and recommend portfolio rebalancing tailored to your actual financial situation.

3. Security, Privacy, and Control: Your Data, Your Terms

It is entirely natural to feel skeptical about a system designed to share your private financial history. However, the Account Aggregator framework was explicitly designed from the ground up to solve the massive security gaps of older methods like email attachments, physical photocopies, and screen-scraping.

The system is built on a “Consent-First” philosophy, enforced through strict architectural safeguards:

- Zero Data Retention: Account Aggregators do not store your data. They act strictly as digital couriers. When your bank sends your statement to a lender, the data passes through the AA app in an encrypted format. The AA cannot decrypt it, read it, or save a copy on its servers.

- Granular Consent: When you receive a data-sharing request on your AA app, it is not an “all-or-nothing” permission. The app displays a clear electronic consent artifact detailing exactly what is being requested.

What you see before approving:

- Who is asking: The specific name of the regulated institution.

- What they want: The specific data type (e.g., “Bank Statement transactions, not your balance”).

- Why they need it: The explicit purpose (e.g., “Home Loan Assessment”).

- How long they can see it: A strict time window (e.g., “One-time pull” or “Monthly access for 6 months”).

- The Power to Revoke: If you grant a personal finance app ongoing access to view your mutual fund balances monthly, you retain the right to revoke that consent at any moment. The moment you hit “Revoke” in your AA app, the data pipeline shuts down instantly.

4. Step-by-Step Guide: How to Get Started with an Account Aggregator

Registering for an Account Aggregator is completely voluntary, free of charge for consumers, and takes less than five minutes.

Step 1: Choose and Download an AA app:

Download an RBI-licensed Account Aggregator app from the Google Play Store or Apple App Store. You can also register directly through the settings menu of many major banking and investment apps.4

Step 2: Create Your Unique AA Handle:

Sign up using the mobile number linked to your bank accounts. You will create a simple, unique identifier known as an AA Handle (for example, yourname@handle). This works exactly like your UPI ID.

Step 3: Link Your Financial Accounts:

The app will use your mobile number to search for active accounts across live banks, insurance providers, and mutual fund depositories. You will see a list of your accounts; verify them using an OTP sent by your respective bank or financial institution to securely link them to your AA handle.

Step 4: Manage and Share on Demand:

Your setup is complete. The next time you apply for a loan or use a wealth management platform, provide your AA Handle. You will receive a push notification on your AA app, where you can inspect the request and tap to share your data securely.

Common Myths vs. Reality

- Myth: “AAs can withdraw money from my account.” Reality: The AA framework is exclusively a data-sharing network. It has absolutely no integration with payment gateways or money transfer protocols. It is structurally impossible for an AA app to move, withdraw, or invest your funds.

- Myth: “Once I sign up, all my data is automatically shared.” Reality: No data ever moves automatically. Every single transfer requires an explicit, active OTP confirmation or biometric approval from you for that specific transaction.

Conclusion: Take Charge of Your Financial Data

The Account Aggregator framework marks a fundamental shift in economic power. For decades, financial institutions held your data behind closed walls, making it difficult for you to leverage your own clean repayment histories and investment records to secure better loans or smarter financial advice.

By acting as a secure, data-blind courier, the AA system eliminates tedious paperwork, drastically reduces processing times, and protects you from the privacy risks of sharing unencrypted files over email and chat apps. Your financial history is an asset. The AA framework gives you the key to use that asset on your own terms.

If you haven’t already, consider downloading a regulated Account Aggregator app today, creating your personal handle, and taking full control of your digital financial footprint.