This podcast episode is based on this article and Audio created using NotebookLM.

Every day, we make money decisions. We decide how much to spend and how much to save. We think about taking loans or investing money. These choices affect our comfort today and our security in the future.

However, many people make these decisions without fully understanding money. This is why financial literacy is important.

In a fast-growing country like India, digital payments, loans, investments, and financial apps are everywhere. Knowing how money works is no longer a luxury. Financial literacy is now a basic life skill.

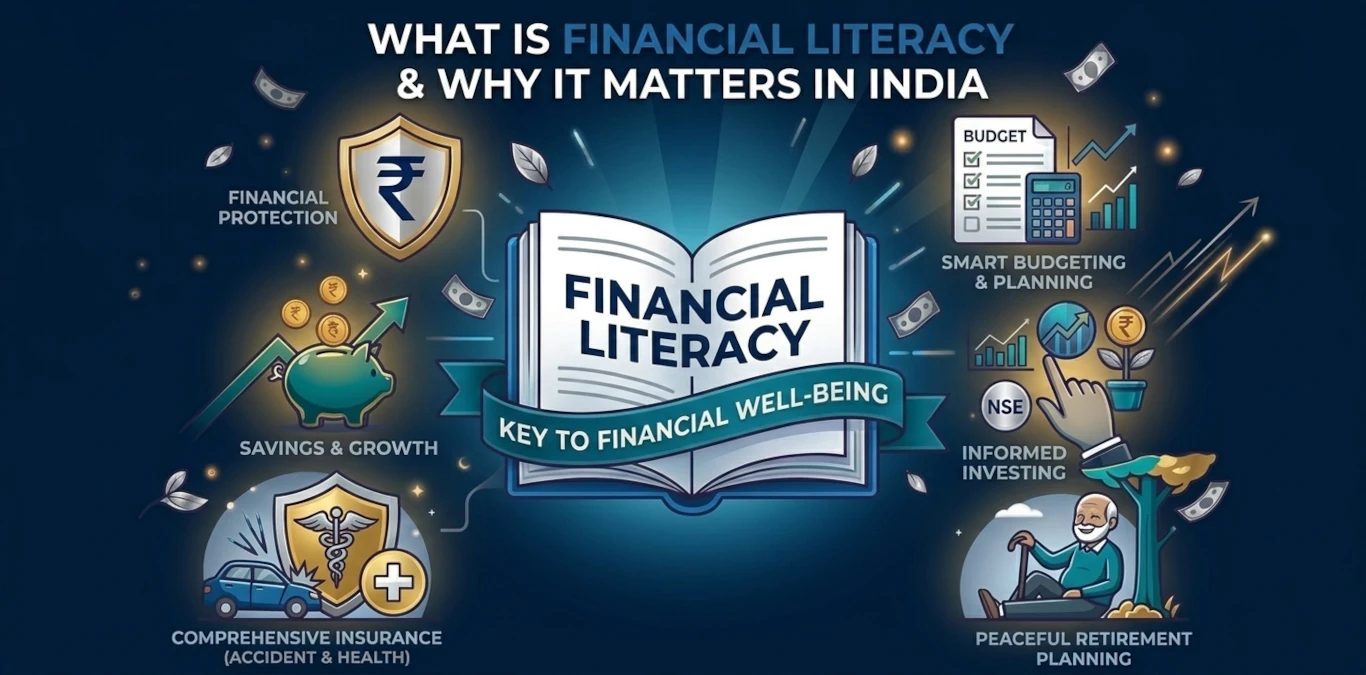

What Is Financial Literacy?

According to the OECD, financial literacy means:

A combination of awareness, knowledge, skills, attitudes, and behaviours necessary to make sound financial decisions and ultimately achieve individual financial well-being.

In simple words, financial literacy means:

- Understanding basic ideas like interest, inflation, and risk

- Knowing how financial products work, such as bank accounts, insurance, mutual funds, and pensions

- Having the skills to manage money well

- Developing responsible money habits and behaviour

However, this definition is incomplete unless we connect it to real-life behavior.

Understanding interest rates, for example, does not automatically prevent someone from taking an expensive loan. But comparing the total repayment amount before borrowing—that is financial literacy in action.

To put it simply, financial literacy is not about knowing terms. It is about making better decisions at the exact moment when money is involved.

Why Financial Literacy Matters in India

India has undergone a massive financial transformation in recent years. The combination of access and convenience has created new opportunities. But it has also introduced new risks.

Let’s imagine giving someone a car for the first time. If they know how to drive, it becomes a powerful tool. If they don’t, it becomes dangerous. Financial tools work in the same way.

1. Low Financial Awareness Despite High Financial Access

India has made strong progress in financial inclusion. Schemes like Jan Dhan Yojana, UPI, and Direct Benefit Transfers have helped millions open bank accounts and use digital payments.

But access alone is not enough.

Many people:

- Have bank accounts but do not use them properly

- Use UPI and apps without knowing how to avoid fraud

- Buy financial products without understanding costs, returns, or risks

Financial literacy helps people use financial services correctly and confidently, not just access them.

2. Better Control Over Loans and Debt

Nowadays, many Indian households use personal loans, credit cards, and Buy Now, Pay Later options. Without proper knowledge, this can lead to too much borrowing and heavy interest payments. It can also cause debt stress.

Financial literacy helps people plan budgets, understand loan terms, compare interest rates, and borrow wisely. This reduces financial pressure and improves stability.

3. Smarter Saving and Future Planning

Indians have a strong habit of saving. However, much of this money is still kept in cash, gold, or low-return options. These choices are safe, but relying only on them limits growth.

Financial literacy encourages people to spread savings across different options. It helps them invest based on goals, time period, and risk level. It also explains the importance of long-term investing, retirement planning, and the impact of inflation over time.

This is especially important as people live longer and family support systems continue to change.

4. Safe Use of Digital and Fintech Services

India is also a global leader in digital payments and financial technology, which has made financial services more accessible than ever before. At the same time, digital finance brings risks such as online fraud, data misuse, and fake investment schemes.

Financially literate individuals are better equipped to identify scams, protect their personal information, and choose suitable financial products. Financial literacy therefore plays a crucial role in ensuring safe and confident participation in the digital economy.

The Gap Between Knowing and Doing

Most people assume that once they understand financial concepts, they will automatically make better decisions. In reality, this rarely happens.

Consider a common situation. You are shopping online, and you see an option to “Buy Now, Pay Later.” The monthly installment looks small, only ₹500. At that moment, you are not calculating the total cost or thinking about interest rates. You are reacting to affordability in the present.

This happens because financial decisions are often driven by behavior, not knowledge.

Modern apps are designed to reduce friction. Saved payment details, one-click checkout, and instant approvals make spending effortless. The easier it becomes to spend, the harder it becomes to pause and think.

Financial Literacy and India’s Growth

When citizens understand money better, the whole country benefits. Financially aware people:

- Make smarter economic decisions

- Depend less on government support

- Strengthen the financial system

India’s National Strategy for Financial Education (NSFE) follows global OECD guidelines and recognises financial literacy as the foundation of financial well-being and economic stability.

Conclusion

Financial literacy does not mean becoming a finance expert. It means being aware, confident, and responsible with money.

As India moves towards a digital and investment-driven economy, financial literacy will decide whether people grow with the system—or struggle within it. Building financial literacy is not just a personal goal; it is a shared responsibility for families, educators, institutions, and society as a whole.