When most people think about financial planning, their minds immediately jump to the “exciting” stuff: picking the next breakout stock, watching their mutual fund dividends roll in or flipping a property for profit. It’s natural to want to focus on growth. However, if you build a skyscraper on a swamp without driving down foundational pilings first, that building will sink.

In the world of finance, insurance is that piling.

Before you build wealth, you must protect it.

Financial planning is not just about returns. It is about resilience. It is about ensuring that an unexpected event, such as a medical emergency, accident, disability or untimely death of a breadwinner, does not wipe out years of savings. Such events should not derail your family’s future.

Insurance is the shock absorber of your financial life. Without it, your investment plan stands on unstable ground. It does not promise high returns or quick gains. But it performs a far more fundamental role: it protects you from financial collapse when life takes an unexpected turn. In fact, insurance is the foundation upon which every sound financial plan is built.

Today, we are going to look into why insurance is the undisputed first step in your journey. Why skipping it to jump straight into investing is the most common and dangerous mistake young professionals and families make.

Understanding Financial Planning: Why Protect Before Build

Financial planning has two major components:

- Risk Management (Protection)

- Wealth Creation (Growth)

Most people focus only on the second part. But growth without protection is fragile.

Let’s imagine you are building a fortress. You have limited resources. Do you spend all your gold on gold-plated thrones and tapestries for the inner chambers first? Or do you build the moat, the thick stone walls and the watchtowers?

Investing is the gold-plated throne. It’s what makes the interior of your life comfortable and luxurious over time. Insurance is the moat and the walls. Without the walls, a single “raid” (a medical emergency, a car accident or the loss of a breadwinner) allows the outside world to come in and strip away every bit of gold you’ve worked so hard to accumulate.

Without risk management, your investments are exposed. A single crisis can force you to liquidate mutual funds, sell stocks at a loss, break fixed deposits or even take on high-interest debt.

Understanding Insurance: What It Really Is

At its core, insurance is a risk management tool. Insurance does not create wealth. It protects wealth. Most people view insurance through the lens of cost (the premium). Financial experts view it through the lens of risk transfer.

Life is unpredictable. Illness, accidents, natural disasters, disability or death can occur without warning. These events can create sudden and massive financial burdens. Insurance works by transferring that financial risk from an individual to an insurance company.

Let’s look at the math of disaster: If you have ₹5,00,000 in a savings account intended for your child’s education and a medical emergency costs ₹6,00,000, your “investment” for your child is gone instantly. You are back to zero or worse, in debt. If you had a health insurance policy with a premium of ₹15,000 a year, that ₹5,00,000 remains untouched. You didn’t “lose” ₹15,000; you “saved” ₹5,00,000.

When you buy insurance, you transfer financial risk to an insurance company in exchange for a premium. If a defined adverse event occurs, the insurer bears the financial burden. Insurance protects you from low-probability, high-impact events. These events can permanently damage financial stability.

Investments grow money slowly over time. Insurance protects you instantly from catastrophic loss. That is why insurance comes first.

The Psychological Value: Peace of Mind

Financial planning is not just mathematical; it is highly emotional. Financial stress almost always stems from uncertainty, the nagging “What ifs” of life:

- What if I fall sick and a hospital bill destroys my savings?

- What if an accident forces me into debt?

- What if something happens to me and my family loses their income?

When you have comprehensive insurance (Life, Health and Disability), you silence those questions and gain a psychological superpower: The Ability to Stay the Course.

Knowing that your family is taken care of and that your financial “floor” is secured reduces your anxiety. It allows you to make logical, rather than fear-based, decisions. You invest more confidently, you stay invested during market volatility and you can even afford to take calculated, long-term risks with your portfolio. This peace of mind may not be measurable in direct returns but it is the ultimate foundation for financial discipline.

Key Types of Insurance You Should Prioritize

Different types of insurance protect different areas of life. Here are the core insurance products that form the foundation of financial planning.

1. Term Life Insurance: The Ultimate Love Letter

For anyone with dependents (spouse, children, aging parents), life insurance is non-negotiable. We specifically advocate for Term Insurance. It is pure protection: you pay a small premium for a large cover.

- The “Why”: If the primary earner passes away, the investments usually aren’t enough to cover 20 years of lost income. Life insurance fills that gap instantly, ensuring the family can stay in their home and the children can finish school.

2. Health Insurance: Protecting Your Liquid Cash

Medical inflation is currently outpacing general inflation. A single specialized surgery can wipe out three years of diligent SIP (Systematic Investment Plan) contributions.

- The “Why”: Health insurance ensures that your “Investment Bucket” and your “Emergency Bucket” remain separate. You use the insurance company’s money for the hospital, leaving your wealth to continue compounding.

3. Personal Accident & Disability Insurance: The Forgotten Shield

What happens if you survive an accident but can no longer work? This is often more financially devastating than death because the living expenses continue (and often increase due to care needs) but the income stops.

- The “Why”: Disability insurance provides a replacement income or a lump sum that allows you to modify your life and home without draining your retirement fund.

4. Motor Insurance (Mandatory but Crucial)

Motor insurance is legally mandatory in India. But beyond compliance, it protects you from:

- Large repair costs

- Third-party liabilities

- Legal complications

A serious accident can create financial liability far beyond the value of your vehicle.

Real-Life Scenario: A Tale of Two Professionals

Let’s look at “Rahul” and “Priya,” both 30-year-old managers earning similar salaries.

- Rahul decides to put every spare Rupee into the stock market. He wants to “fire” (Financial Independence, Retire Early). He skips insurance because he “knows how to manage his money.”

- Priya decides on a balanced approach. Before she buys her first mutual fund, she secures a ₹1 Crore Term Life policy and a ₹10 Lakh Health cover. It costs her about ₹2,000 a month.

Three years later, both have a major health scare requiring a ₹5 Lakh surgery.

- Rahul has to sell his stocks. Unfortunately, the market is currently down 15%. He sells at a loss, loses his compounding momentum and feels a massive amount of stress.

- Priya calls her TPA (Third Party Administrator). The insurance pays the hospital directly. Her investments remain untouched, continuing to grow through the market dip.

Who is closer to financial freedom?

Priya. Because her path was linear, while Rahul’s was interrupted.

Why Insurance Must Come Before Investing

Let’s look at the chronological logic. If you start investing ₹10,000 a month today into a diversified equity fund, after one year, you have ₹1.2 Lakh (plus growth).

If a catastrophe hits in Month 13:

- Without Insurance: You liquidate your ₹1.2 Lakh. It’s likely not enough. You take a loan. Your financial plan is now in the “negative.”

- With Insurance: You pay your small premium. Your ₹1.2 Lakh stays in the market. It continues to grow. You have effectively “outsourced” your catastrophe to an insurance company.

Investing is for your “Best Case Scenario” (Retirement, wealth, dreams). Insurance is for your “Worst Case Scenario.” You cannot safely plan for the best until you have mitigated the worst.

1. You Cannot Grow Wealth If It Is Not Protected

Investing without insurance is like driving without a seat-belt because you are confident in your driving skills. You may drive safely for years until one accident changes everything.

Insurance ensures that your financial plan survives unexpected shocks.

2. Insurance Protects Your Compounding Momentum

The real magic of wealth creation is compound interest, only works if you leave your money alone to grow over time. When a crisis hits without insurance, as we saw with Rahul, you are forced to liquidate your investments to cover the emergency. This not only resets your compounding clock back to zero but if the market is down, it forces you to sell at a loss.

Insurance acts as a financial firewall around your portfolio. By transferring the cost of an emergency to an insurance company (like Priya did), your investments remain completely untouched. They get to stay in the market, riding out the dips and continuing to compound undisturbed. You cannot build long-term wealth if you constantly have to break into your own vault to survive.

3. Investing Carries Market Risk – Insurance Does Not

Markets fluctuate. Investments can go up and down. In some years, returns may be negative.

Insurance is not dependent on market performance. If the insured event occurs, the policy pays out as per the contract terms.

This reliability makes insurance the stabilizing component of your financial plan.

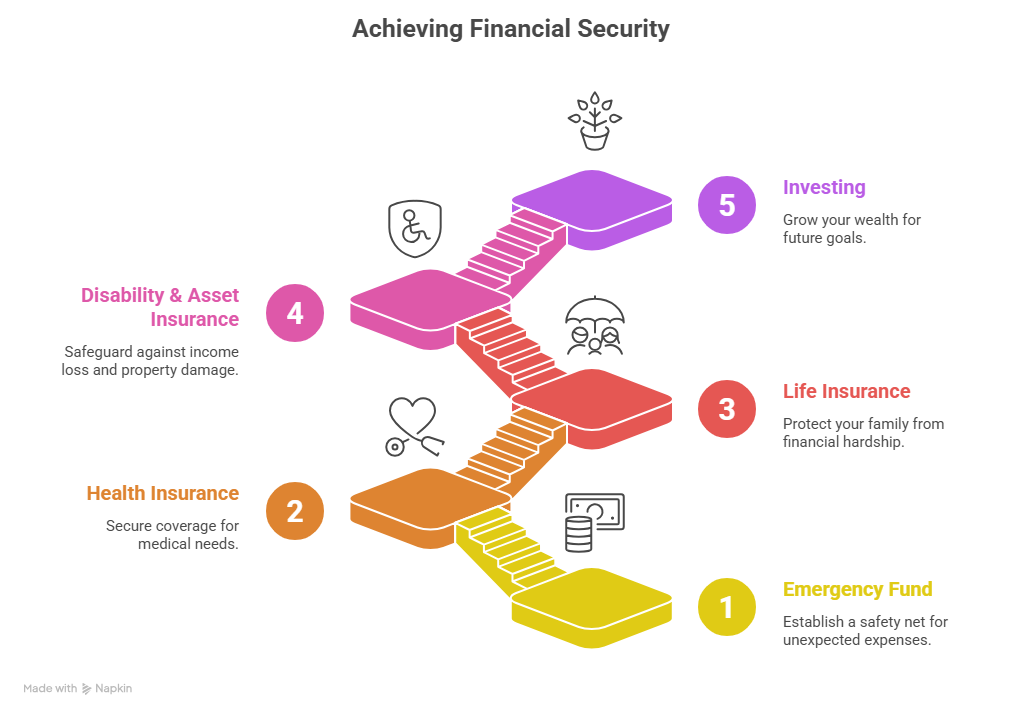

How to Structure Your Financial Plan

For young professionals and families, the ideal sequence is:

- Build a small emergency fund (3–6 months of expenses).

- Buy adequate health insurance.

- Buy term life insurance.

- Consider disability and asset insurance as needed.

- Then begin investing for goals.

Why this order?

Because investing without risk protection is like driving fast without wearing a seat-belt.

You may not crash but if you do, the damage is severe.

Insurance vs. Investment: Understanding the Difference

One common misconception is that insurance and investment are interchangeable. They are not. Let’s break it down clearly.

| Feature | Insurance | Investment |

| Purpose | Protection against financial loss. | Wealth creation and capital growth. |

| Outcome | Pays out only if a specific event occurs. | Grows over time based on market performance. |

| Risk | Reduces your overall financial risk. | Involves taking on risk in pursuit of returns. |

When people say, “I prefer investing over buying insurance,” they are mixing two completely different financial tools. It is not insurance versus investment. It is insurance first, then investment.

Conclusion: Protect First, Then Grow

Financial literacy is about more than just numbers; it’s about stewardship. It’s about being a good steward of your family’s future and your own hard work.

By prioritizing insurance, you are making a profound statement: “I value my future enough to protect it.” You are ensuring that no matter what life throws your way (be it a health crisis, an accident or an untimely passing) your financial goals will remain intact.

Don’t wait until you have “enough money” to get insured. Insurance is the tool that allows you to accumulate enough money without the fear of it being snatched away. Insurance does not eliminate risk but it reduces the financial impact of that risk.

Insurance may not be glamorous. It does not create excitement like stock market gains.

But it creates something far more valuable: Financial security. And financial security is the true starting point of financial freedom. When protection comes first, growth becomes sustainable.

That is sound financial planning.

Your Next Step: Before you check your portfolio or look at the latest market trends today, pull out your insurance documents. Do you have a Term plan? Is your Health cover sufficient for today’s medical costs? If not, make that your priority this week.

Once the foundation is poured and the walls are up, then and only then, it is time to start decorating the interior of your financial fortress.